Posts Tagged ‘capitalism’

“The violence of positivity does not deprive, it saturates; it does not exclude, it exhausts”*…

Scheduling note: your correspondent is hitting the road again, so regular service will be interrupted; it should resume on Friday the 7th…

Author and psychoanalyst Josh Cohen on Byung-Chul Han’s critiques of digital capitalism…

I came across Byung-Chul Han towards the end of the previous decade, while writing a book about the pleasures and discontents of inactivity. My first researches into our culture of overwork and perpetual stimulation soon turned up Han’s The Burnout Society, first published in German in 2010. Han’s descriptions of neoliberalism’s culture of exhaustion hit me with that rare but unmistakable alloy of gratitude and resentment aroused when someone else’s thinking gives precise and fully formed expression to one’s own fumbling intuitions.

At the heart of Han’s conception of a burnout society (Müdigkeitsgesellschaft) is a new paradigm of domination. The industrial society’s worker internalises the imperative to work harder in the form of superego guilt. Sigmund Freud’s superego, a hostile overseer persecuting us from within, comes into being when the infantile psyche internalises the forbidding parent. In other words, the superego has its origin in figures external to us, so that, when it tells us what to do, it is as though we are hearing an order from someone else. The achievement society of our time, Han argues, runs not on superego guilt but ego-ideal positivity – not from a ‘you must’ but a ‘you can’. The ego-ideal is that image of our own perfection once reflected to our infantile selves by our parents’ adoring gaze. It lives in us not as a persecutory other but as a kind of higher version of oneself, a voice of relentless encouragement to do and be more.

With this triumph of positivity, the roughness of the demanding boss gives way to the smoothness (a key Han term) of the relentlessly encouraging coach. On this view, depression is the definitive malaise of the achievement society: the effect of being always made to feel that we’re running hopelessly behind our own ego-ideal, exhausting ourselves in the process.

The figure of the achievement subject gives rise to some of Han’s most vivid evocations of psychic and bodily debilitation:

The exhausted, depressive achievement-subject grinds itself down … It is tired, exhausted by itself, and at war with itself. Entirely incapable of stepping outward, of standing outside itself, of relying on the Other, on the world, it locks its jaws on itself; paradoxically, this leads the self to hollow and empty out. It wears out in a rat race it runs against itself…

… Han’s critique of contemporary life centres on its fetish of transparency; the compulsion to self-exposure driven by social media and fleeting celebrity culture; the reduction of selfhood to a series of positive data-points; and the accompanying hostility to the opacity and strangeness of the human being…

… Under the rule of digital capitalism, time itself is severed from any ‘narrative or teleological tension’, that is, from any discernible purpose or meaning, and so, like the digital paintings in an immersive show, it ‘disintegrates into points which whizz around without any sense of direction.’ In such a regime of time, there is no possibility of Erfahrung, which depends on a sense of narrative continuum and duration. There is only the proliferation of its pale counterpart Erlebnis: the discrete event that ‘amuses rather than transforms’, as Han would later put it in The Palliative Society…

… Because power so often involves coercion, Han argues, there has been a tendency to see them as inextricable. But it is only when power is poor in mediation, felt as alien to our own lives and interests, that it resorts to threatened or actual violence. Whereas when power is at the ‘highest point of mediation’ – when it seems to speak from a recognition of its subjects’ needs and desires – it is more likely to receive those subjects’ willing consent. One could conceive of a power, therefore, that has no sanctions at its disposal, but which is nonetheless rendered absolute by its subjects’ full identification with it.

The less it relies on the threat of punitive measures to back it up, the more power maximises itself. ‘An absolute power,’ writes Han, ‘would be one that never became apparent, never pointed to itself, one that rather blended completely into what goes without saying.’ This is precisely what happens in digital capitalism’s burnout society, where the power of capital consists not in its power to oppress but in the voluntary surrender of its subjects to their own exploitation.

Han draws on the German-American theologian Paul Tillich’s conception of power as ipsocentric, that is, as Han puts it, centred around ‘a self whose intentionality consists of willing-itself’, cultivating and bolstering its own status. God is the ultimate embodiment of power because, in the words of G W F Hegel, ‘he is the power to be Himself’. This will to persist in one’s own existence, to cling to one’s own selfhood, is the basic premise of the Western mode of being. We can discern it at work in the empty narcissism of social media and the culture of self-display in which we’re all enjoined to participate. Self-exploitation is, in a sense, a twisted variant on the Cartesian cogito: I am seen therefore I am. In making myself perpetually visible, I may empty myself out, lose the last vestiges of my interiority. But, in cleaving to the bare bones of a self-image, some form of my existence survives.

The fundamental basis of this erosion of meaningful experience, argues Han, is felt at the level of temporality. The accelerated time of digital capitalism effectively abolishes the practice of ‘contemplative lingering’. Life is felt not as a temporal continuum but as a discontinuous pile-up of sensations crowding in on each other. One of the more egregious consequences of this new temporal regime is the atomisation of social relations, as other people are reduced to interchangeable specks in the same sensory pile-up. Trust between people, grounded in both the assumption of mutual continuity and reliability, and in a sense of knowing the other as singular and distinct, is inexorably corroded: ‘Social practices such as promising, fidelity or commitment, which are temporal practices in the sense that they commit to a future and thus limit the horizon of the future, thus founding duration, are losing all their importance.’…

Consumer culture, with its compulsion for novelty and perpetual stimulation, likewise erodes the bonds of shared experience that engender meaningful narratives. The fire around which human beings would once have gathered to hear stories has been displaced by the digital screen, ‘which separates people as individual consumers.’ Time, love, art, work, narrative; these are the key zones of experience hollowed out by the disintegrative logic of digital capitalism. Each is a rich store of transformative encounter, or Ehrfahrung, which the ‘non-time’ of the present has reduced to empty instances of Erlebnis…

How the “suffocating system” of digital capital creates hollowed-out lives: “The winter of civilization,” the thought of @byungchulhan.bsky.social in @aeon.co. Eminently worth reading in full.

* Byung-Chul Han, The Burnout Society

###

As we analyze ambition, we might send careful birthday greeting to Charles Ponzi; he was born on this date in 1882. A con artist, he swindled his way across Canada and the U.S. in the early 1920s, promising clients a 50% profit within 45 days or 100% profit within 90 days, by buying discounted postal reply coupons in other countries and redeeming them at face value in the U.S. as a form of arbitrage. In reality, Ponzi was paying earlier investors using the investments of later investors. While this type of fraudulent investment scheme wasn’t invented by Ponzi, it became so identified with him that it now is referred to as a “Ponzi scheme“. The scam for which he’s known ran for over a year before it collapsed, costing his “investors” $20 million (over $300 million at current value).

Ponzi schemes have grown since Ponzi’s time (Bernie Madoff‘s version is estimated to have totalled around $65 billion) and are alive and well in the U.S.

“There’s class warfare all right, but it’s my class, the rich class, that’s making war, and we’re winning”*…

Trevor Jackson on Martin Wolf‘s new book, The Crisis in Democratic Capitalism, and a fundamental question it raises: if globalization has allowed elites to remove themselves from democratic accountability and regulation, is there any path toward a just economy?…

Something has gone terribly wrong. In his 2004 book Why Globalization Works, the economics journalist Martin Wolf wrote that “liberal democracy is the only political and economic system capable of generating sustained prosperity and political stability.” He was articulating the elite consensus of the time, a belief that liberal democratic capitalism was not only a coherent form of social organization but in fact the best one, as demonstrated by the West’s victory in the cold war. He went on to argue that critics who “complain that markets encourage immorality and have socially immoral consequences, not least gross inequality,” were “largely mistaken,” and he concluded that a market economy was the only means for “giving individual human beings the opportunity to seek what they desire in life.”

Wolf wrote those words midway through a four-decade global expansion of markets. Throughout the 1980s in Britain, the United States, and France, governments led by Margaret Thatcher, Ronald Reagan, and François Mitterrand set about privatizing public assets and services, cutting welfare state provisions, and deregulating markets. At the same time, a set of ten policies known as the “Washington Consensus” (because they were shared by the International Monetary Fund, the World Bank, and the US Treasury) brought privatization, liberalization, and globalization to Latin America following a series of sovereign debt crises. In the 1990s a similar set of policies, then known as “shock therapy,” suddenly converted the formerly Communist economies of Eastern Europe and the Soviet Union to free markets. Around the Global South, and especially in the rapidly industrializing countries of East Asia after the 1997 financial crisis, “structural adjustment” policies that were conditions for IMF bailouts again brought liberalization, privatization, and fiscal discipline. The same policies were enforced on the European periphery after 2009, in Portugal, Ireland, Italy, Greece, and Spain, again, either as conditions for bailouts or through EU fiscal restrictions and restrictive European Central Bank policy. Today there are far more markets in far more aspects of human life than ever before.

But the sustained prosperity and political stability that these policies were meant to create have proved elusive. The global economy since the 1980s has been riven by repeated financial crises. Latin America endured a “lost decade” of economic growth. The 1990s in Russia were worse than the Great Depression had been in Germany and the United States. The austerity and high-interest-rate policies after the 1997 East Asia crisis restored financial stability but at the cost of domestic recessions, and contributed to political instability and the repudiation of incumbent parties in Indonesia, the Philippines, and South Korea, as they did again across Europe after 2009–2010. Global economic growth rates in the era of globalization have been about half what they were in the less globalized postwar decades. Around the world, violent racist demagogues keep winning elections, and although they all seem very happy with the idea of private property, they are openly hostile to the rule of law, political liberalism, individual freedom, and other ostensible preconditions and cultural accompaniments to market economies. Both democracy and globalization seem to be in retreat in practice as well as in ideological popularity. Or, as Wolf writes in his new book, The Crisis of Democratic Capitalism:

Our economy has destabilized our politics and vice versa. We are no longer able to combine the operations of the market economy with stable liberal democracy. A big part of the reason for this is that the economy is not delivering the security and widely shared prosperity expected by large parts of our societies. One symptom of this disappointment is a widespread loss of confidence in elites.

What happened?

Martin Wolf is probably the most influential economics commentator in the English-speaking world. He has been chief editorial writer for the Financial Times since 1987 and their lead economics analyst since 1996. Before that he trained in economics at Oxford and worked at the World Bank starting in 1971, including three years as senior economist and a year spent working on the first World Development Report in 1978. This is his fifth book since moving to the Financial Times. The blurbs and acknowledgments are stuffed with central bankers, financiers, Nobel laureates, and celebrity academics. The bibliography contains ninety-six references to the author himself.

Wolf’s diagnosis is impossible to dispute: “Neither politics nor the economy will function without a substantial degree of honesty, trustworthiness, self-restraint, truthfulness, and loyalty to shared political, legal, and other institutions.” But, he observes, those values have run into crisis all over the world, and, especially since about 2008,

…people feel even more than before that the country is not being governed for them, but for a narrow segment of well-connected insiders who reap most of the gains and, when things go wrong, are not just shielded from loss but impose massive costs on everybody else…

He describes in detail the mistaken policies of austerity in the US and Europe, the rise of a wasteful and extractive financial sector, the atomization and immiseration of formerly unionized workers, the pervasiveness of tax avoidance and evasion, and the general accumulation of decades of elite failure…

Read on for Wolf’s proposed remedies and Jacksons critiques: “Never Too Much,” from @nybooks.com.

And for an interview with Jackson that elaborates on his thoughts and their historical context, see here.

* Warren Buffett

###

As we assess systems, we might send provocative birthday grretings to Founding Father Thomas Paine; he was born on this date in 1736 (O.S.; on February 9, 1737 per N.S., which accrued in Britain and its colonies in 1752). He is best known for Common Sense and The American Crisis, two influential pamphlets that helped to inspire colonial era American patriots in 1776 to declare independence from Great Britain.

But relevantly to the article above, in 1797 (after witnessing the birth and early years of the U.S. and spending time in France) he wrote Agrarian Justice, in which he proposed remedies for several of the (then nascent) ills discussed by Wolf and Jackson…

In response to the private sale of royal (or common) lands, Paine proposed a detailed plan to tax land owners [the “capitalists” of their day] once per generation to pay for the needs of those who have no land. Some consider this a precursor to the modern idea of citizen’s dividend or basic income. The money would be raised by taxing all direct inheritances at 10%, and “indirect” inheritances, those not going to close relations, at a somewhat higher rate. He estimated that to raise around £5,700,000 per year.

Around two-thirds of the fund would be spent on pension payments of £10 per year to every person over the age of 50, which Paine had taken as his average adult life expectancy.

Most of the remainder would be used to make fixed payments of £15 to every man and woman on reaching the age of 21, then the age of legal majority.

The small remainder of the money raised that was still unused would be used for paying pensions to “the lame and blind.”

For context, the average weekly wage of an agricultural labourer was around 9 shillings, which would mean an annual income of about £23 for an able-bodied man working throughout the year.

Paine’s proposal presaged the social safety net of later eras and governments, proposing seven entitlements to protect the poorest citizens from the ravages of market capitalism:

- Grants to subsidize schooling of 4 pounds per annum

- One-time payments to adults on reaching maturity

- One-time payments to newly married couples and new parents

- Eliminate taxes on working poor

- Back-to-work schemes

- Pensions for seniors

- Burial benefits to surviving spouses

and also provided a scheme of how to pay for them.

– source

“It’s easier to imagine the end of the world than the end of capitalism”*…

… so it’s useful to contemplate its beginning. David Rooney, in an excerpt from his book About Time…

Ömer Aga stood in the middle of Amsterdam’s Dam Square surrounded by his nineteen-strong party of advisers, interpreters and hosts, and gazed toward the huge new trading exchange that straddled the mighty Rokin canal, just to the south of the square. The year was 1614, and Aga was on a fact-finding mission to the Dutch Republic as the Ottoman Empire’s newest diplomatic emissary. Top of his list of must-see sights was this bold new building, completed just three years earlier. It was hard to miss, as it was the size of a soccer field and could accommodate thousands of traders in its 200-by-115-foot enclosed inner courtyard, but what Aga really noticed was the four-sided clock tower that loomed over the vast structure and the streets and canals all around, as well as the booming sound of its bell when they rang out the hours and then, at noon, tolled repeatedly for a few minutes before falling silent. Little did they realize it, but Omar Aga and his retinue were listening to one of the most significant clocks ever made. It was fitted to the world’s first stock exchange and sounded the birth of modern capitalism.

From the moment the Amsterdam exchange building first opened its doors in August 1611, traders were forbidden from trading anywhere else in the city. But the exchange did not just put spatial boundaries on trade. It concentrated traders in time, too. A few days before the new facility opened, the city council had issued a bylaw proclaiming that trading could only take place between the hours of 11 a.m. and noon, Monday to Saturday. At noon, the clock installed in the tower high above the exchange building would toll a bell for seven and a half minutes. If any traders were still in the exchange, or in the streets nearby, they would be fined. Additionally, trading was allowed between 6:30 p.m. and 7:30 p.m. during the summer months between May and August, and in winter evening trading took place for a thirty-minute period marked by a tolling bell at the city’s gates. At the end of evening trading, the exchange clock would again sound for seven and a half minutes and fines were issued for anyone caught trading after the bells fell silent.

Why were such strict limits placed on trading at the Amsterdam exchange? There were several reasons. One was a practical problem familiar to anybody involved with trade in a busy city center: time limits reduced congestion and disruption in the streets nearby. Another was that clocks made trading more efficient. Short, fixed trading hours concentrated buyers and sellers together, making it easier for each to find enough of the other. This increased the volume of trade, which was good for traders and for the city council collecting taxes on transactions. But clocks also helped prices to remain fair, as they could be used to regulate the people who occupied intermediate roles in the functioning of a market.

Some of the earliest references to mechanical clocks being used in towns and cities, in the Middle Ages and soon after, related to market restrictions. The first urban markets brought producers of food, cloth and so on into direct contact with the consumers of their wares. But as towns and cities grew, this model started to break down. It stopped making sense for every producer in the countryside to make the journey all the way to the center of towns. So, ‘intermediate trading’ emerged, whereby third parties might buy up the goods from several small producers somewhere on the edge of town, before bringing them in and selling them themselves at the market. Soon, a whole range of intermediate roles sprang up. Wholesalers, merchants, shopkeepers and peddlers were some, but intermediates also included financiers who advanced funds, and those speculating on the future in the hope of offsetting risk (whether because of bad harvests or other unpredictable events) and making more money. Some people occupied more than one role.

As populations grew and moved in increasing numbers to towns and cities, and markets began to sell more and more products, the rise of intermediate roles in market-based trade was inexorable, creating a new stratum of people who neither produced goods nor consumed them, but traded, speculated, brokered, hoarded, flipped and financed. Some market authorities feared intermediates would drive up prices or limit supplies and turned to clocks to control their involvement. Clocks meant that different groups could be treated differently at the market. In a sixteenth-century grain market, for instance, the first hours of trade could be restricted to residents, before bakers of bread could get in, and then the pastry bakers could enter. Only after several hours were wholesalers and other intermediate traders allowed in. But as societies and their market trading became ever more complex, the role of intermediates like brokers and financiers became increasingly important in keeping the flow of trading running smoothly. And, before long, finance became something that could be traded in its own right, and clocks took on a new regulatory role.

Amsterdam’s was not the first trading exchange. Antwerp and London had had exchanges since the sixteenth century where goods and money were traded, but Amsterdam was the first of a new kind of exchange: what became the modern securities exchange. As well as being a place to trade in commodities like salt or hides, people could also buy and sell financial assets. It started out as a place to buy and sell shares in the Dutch East India Company, an early joint-stock company and the first with freely tradable shares, but soon was used to trade other company shares, futures contracts and insurance policies as well as becoming the place to go for information about the state of the markets. The financial market had arrived, but its products, and the prices paid for them, which were time-dependent. The time at which each securities transaction was made, or would be enacted in the future, was central to this new type of trading to work fairly, everybody had to agree what time this was. In other words, trading needed time stamps, which is where the exchange clock came into its own. Clocks were no longer about excluding intermediates from the market. In the new exchanges, intermediates were the market — with the clock watching carefully over the whole thing…

The birth of modern capitalism and the role that timekeeping played in its nascence: The Amsterdam Stock Exchange, from @rooneyvision, via the invaluable @delanceyplace.

* Fredric Jameson (also sometimes attributed to Slavoj Žižek)

###

As we examine enterprise, we might recall that it was on this date in 1937 that Sylvan Goldman introduced the first shopping cart in his Humpty Dumpty grocery store in Oklahoma City.

“Never call an accountant a credit to his profession; a good accountant is a debit to his profession.”*…

The estimable Henry Farrell on accountancy as a lens on the hidden systems of the world…

When reading Cory Doctorow’s latest novel, The Bezzle [which your correspondent highly recommends], I kept on thinking about another recent book, Bruce Schneier’s A Hacker’s Mind: How the Powerful Bend Society’s Rules and How to Bend Them Back [ditto]. Cory’s book is fiction, and Bruce’s non-fiction, but they are clearly examples of the same broad genre (the ‘pre-apocalyptic systems thriller’?). Both are about hackers, but tell us to pay attention to other things than computers and traditional information systems. We need to go beneath the glossy surfaces of cyberpunk and look closely at the messy, complex systems of power beneath them. And these systems – like those described in the very early cyberpunk of William Gibson and others – are all about money and power.

What Bruce says:

In my story, hacking isn’t just something bored teenagers or rival governments do to computer systems … It isn’t countercultural misbehavior by the less powerful. A hacker is more likely to be working for a hedge fund, finding a loophole in financial regulations that lets her siphon extra profits out of the system. He’s more likely in a corporate office. Or an elected official. Hacking is integral to the job of every government lobbyist. It’s how social media systems keep us on our platform.

Bruce’s prime example of hacking is Peter Thiel using a Roth IRA to stash his Paypal shares and turn them into $5 billion, tax free.

This underscores his four key points. First, hacking isn’t just about computers. It’s about finding the loopholes; figuring out how to make complex system of rules do things that they aren’t supposed to. Second, it isn’t countercultural. Most of the hacking you might care about is done by boring seeming people in boring seeming clothes (I’m reminded of Sam Anthony’s anecdote about how the costume designer of the film Hackers visited with people at a 2600 conference for background research, but decided that they “were a bunch of boring nerds and went and took pictures of club kids on St. Marks instead”). Third, hacking tends to reinforce power symmetries rather than undermine them. The rich have far more resources to figure out how to gimmick the rules. Fourth, we should mostly identify ourselves not with the hackers but the hacked. Because that is who, in fact, we mostly are….

…

… Still, there are things you can do to fight back. One of the major themes of The Bezzle is that prison is now a profit model. Tyler Cowen, the economist, used to talk a lot about “markets in everything.” I occasionally responded by pointing to “captive markets in everything.” And there isn’t any market that is more literally captive than prisoners. As for-profit corporations (and venal authorities) came to realize this, they started to systematically remake the rules and hack the gaps in the regulatory system to squeeze prisoners and their relatives for as much money as possible, charging extortionate amounts for mail, for phone calls, for books that could only be accessed through proprietary electronic tablets.

That’s changing, in part thanks to ingenious counter hacking. The Appeal published a piece last week on how Securus, “the nation’s largest prison and jail telecom corporation,” had to effectively default on nearly a billion dollars of debt. Part of the reason for the company’s travails is that activists have figured out how to use the system against it…

…

… In other sectors, where companies doing sketchy things have publicly traded shares, activists have started getting motions passed at shareholder meetings, to challenge their policies. However, the companies have begun in turn to sue, using the legal system in unconventional ways to try to prevent these unconventional tactics. Again, as both Bruce and Cory suggest, the preponderance of hacking muscle is owned by the powerful, not those challenging them.

Even so, the more that ordinary people understand the complexities of the system, the more that they will be able to push back. Perhaps the most magnificent example of this is Max Schrems, an Austrian law student who successfully bollocksed-up the entire system of EU-US data transfers by spotting loopholes and incoherencies and weaponizing them in EU courts. Cory’s Martin Hench books seem to me to purpose-designed to inspire a thousand Max Schrems – people who are probably past their teenage years, have some grounding in the relevant professions, and really want to see things change.

And in this, the books return to some of the original ambitions of ‘cyberpunk,’ a somewhat ungainly and contested term that has come to emphasize the literary movement’s countercultural cool over its actual intentions…

One word that never appears in Neuromancer, and for good reason: “Internet.” When it was written, the Internet was just one among many information networks, and there was no reason to suspect that it would defeat and devour its rivals, subordinating them to its own logic. Before cyberspace and the Internet became entangled, Gibson’s term was a synecdoche for a much broader set of phenomena. What cyberspace actually referred to back then was more ‘capitalism’ than ‘computerized information.’

So, in a very important sense, The Bezzle returns to the original mission statement – understanding how the hacker mythos is entwined with capitalism. To actually understand hacking, we need to understand the complex systems of finance and how they work. If you really want to penetrate the system, you need to really grasp what money is and what it does. That, I think, is what Cory is trying to tell us. And so too Bruce. The nexus between accountancy and hacking is not a literary trick or artifice. It is an important fact about the world, which both fiction and non-fiction writers need to pay attention to…

Eminently worth reading in full: “Today’s hackers wear green eyeshades, not mirrorshades,” from @henryfarrell in his invaluable newsletter Programmable Mutter.

###

As we ponder power, we might recall that on this date in 1927, a “counter-hacker” in a different domain, Mae West, was sentenced to jail for obscenity.

Her first starring role on Broadway was in a 1926 play entitled Sex, which she wrote, produced, and directed. Although conservative critics panned the show, ticket sales were strong. The production did not go over well with city officials, who had received complaints from some religious groups, and the theater was raided and West arrested along with the cast. She was taken to the Jefferson Market Court House (now Jefferson Market Library), where she was prosecuted on morals charges, and on April 19, 1927, was sentenced to 10 days for “corrupting the morals of youth.” Though West could have paid a fine and been let off, she chose the jail sentence for the publicity it would garner. While incarcerated on Welfare Island (now known as Roosevelt Island), she dined with the warden and his wife; she told reporters that she had worn her silk panties while serving time, in lieu of the “burlap” the other girls had to wear. West got great mileage from this jail stint. She served eight days with two days off for “good behavior”.

Wikipedia

“Follow the money”*…

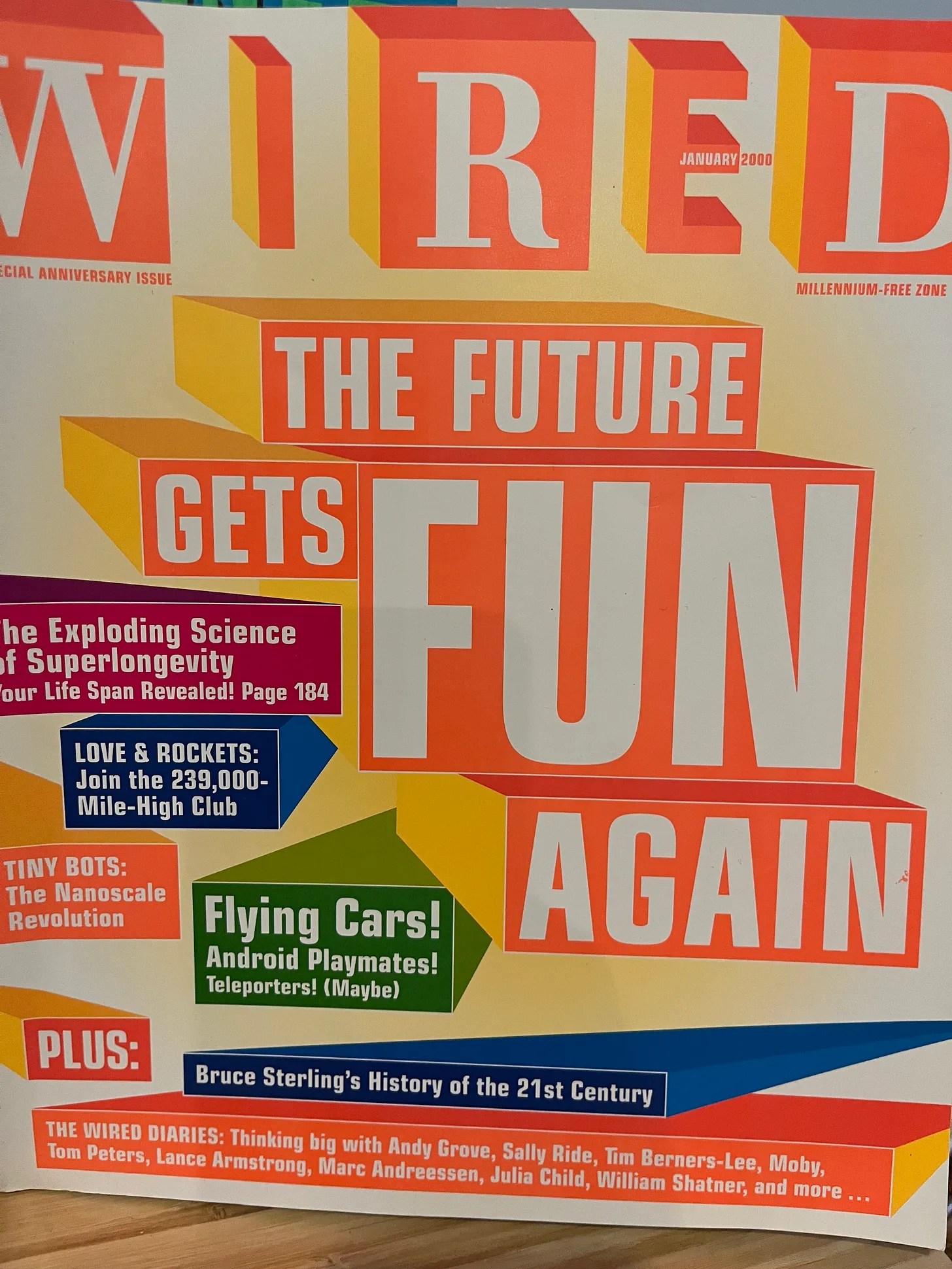

Professor and author Dave Karpf is re-reading the entire WIRED back catalog chronologically (for the second time) for a book project on the “history of the digital future.” A consideration of a 2000 issue devoted to the future has led him to a fascinating insight…

The January 2000 issue is themed around predictions. The magazine did the same thing in January 1999. They ask a ton of experts and celebrities to talk about what the future is going to be like. Some take it seriously, others make jokes. Some are prescient, others notsomuch. It’s a window into what the future looked like back then.

[Karpf reviews a number of the predictions, concluding with…]

…And then there’s this perfect Nathan Myrvhold quote “There won’t be TV per se in three decades. There will be video service over the Internet, but it will be as different from TV today as, say, MTV from the Milton Berle show of the 1950s or from radio plays of the 1940s.”

This is art. I want to frame Myrvhold’s quote and put it in a museum of lopsided tech futurist predictions.

The part that he gets right is the technological development curve. There he is, at the turn of the millennium, five years before the inception of YouTube, telling us that the future of television is going to be video service over the Internet. Yes, absolutely right!

But the part he gets wrong is the industrial, social, and economic impacts of this technological development. We’re seeing this right now, in 2023, as the various streaming services add advertising and strike content-sharing partnership deals with each other. We have these revolutionary new technological developments, and, for about a decade, they were supported by a stock market bonanza. But now that the stocks are no longer ridiculously overvalued, the companies driving these technological developments have settled on a vision of replacing old cable tv with new cable tv. (I wrote about this in July 2022, btw, back when this Substack had a much smaller readership. I think the piece holds up well.)

Technologically, it didn’t have to be this way. But, given all the existing incentive structures established by 21st century capitalism, it was all-but-certain that we would end up here.

I see this time and time again when reading predictions of social transformation from 90s- and 00s-era technologists [cough NicholasNegropontewasconstantlywrong cough]. And I see the same thing today, every time an artificial general intelligence true believer starts opining on the glorious future of education/entertainment/science/manufacturing/art.

I wrote about this phenomenon last year in The Atlantic, where I argued that we won’t be able to tell what the future of AI looks like until we have a sense of where the revenue streams come from. The trajectory of any emerging technology bends towards money.

…

I’m writing a whole book about the lopsided ways in which tech futurists always get their predictions wrong. And one major reason why is that they focus on what the technology could do, given time and mass adoption, rather than considering what capitalism will surely do to those technologies, unless we alter the incentives through regulations.

The trajectory of every emerging technology bends toward revenue streams. If you want to build a better future, you cannot ignore the shaping force of money…

A peek back at some tech predictions from January 2000: “From the WIRED archives: The trajectory of any emerging technology bends toward money,” by @davekarpf (referral account)

See also “The frantic battle over OpenAI shows that money triumphs in the end” (in which Robert Reich argues that, though the revenue streams aren’t yet obvious, protecting their emergence was at the core of the recent battle for control of what was, ostensibly, a not-for-profit) and the oddly apposite “Nerd culture is murdering intellectuals.”

And for more on Karpf’s march through WIRED’s history and what it can tell us about the ways that tech and our culture have changed, see “Notes from #WIRED30.”

* Deep Throat (as portrayed the film adaptation of All the President’s Men)

###

As we pay attention to the profit motive, we might recall that this is an important date in broadcast history. On this date in 1896, Guglielmo Marconi introduced “radio”: he amazed a group at Toynbee Hall in East London with a demonstration of wireless communication across a room. Every time Marconi hit a key beside him at the podium, a bell would ring from a box being carried around the room by William Henry Preece.

Then exactly five years later, on this date in 1901, Marconi confounded those who believed that the curvature of the earth would limit the effective range of radio waves when he broadcast a signal from Cornwall, England to Newfoundland, Canada– over 2,100 miles– and in so doing, demonstrated the viability of worldwide wireless communication.

In the earliest days of radio, when it was essentially a wireless telegraph, there were myriad predictions of what the technology might become– from an internet-like decentralized community of communicators to a provider of education, telemedicine, and other special services… in the event, of course, it followed the money.

You must be logged in to post a comment.