Posts Tagged ‘retailing’

“You all got only three friends in this world: The Lord God Almighty, the Sears Roebuck catalog, and Eugene Talmadge”*…

Our consumer era, born in the mid-19th century, had many parents (e.g., John Wanamaker, who pioneered the department store and helped define the “consumer” and the advertising aimed at him/her). The impetus of the department store– to offer “everything”– has found its modern instantiation in brick and mortar operations like WalMart and Target Superstores, and of course, in the on-line behemoth Amazon, which makes an extraordinary range of goods available to shoppers regardless of their proximity to a physical store.

Leo DeLuca reminds us that, over a century before Amazon, the Sears Catalog played that same role. It reigned supreme for over a century… and offered some odd products…

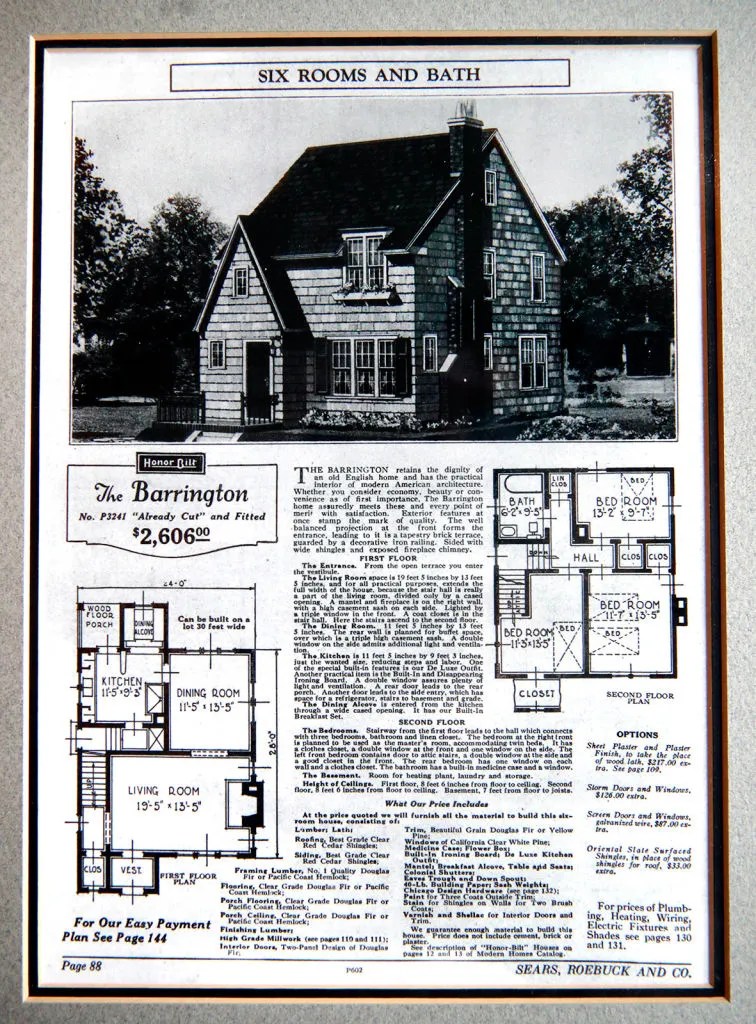

From heroin to houses, Sears had it all. But before the Chicago business became America’s largest retailer—and affixed its name to the world’s tallest building—Sears started by selling time.

In 1886, a 22-year-old station agent on the Minneapolis and St. Louis Railway purchased a shipment of unwanted gold watches from a local jeweler. Wristwatches had just hit the market, and since station agents needed to track train schedules, the young man thought he might hawk the watches to his fellow railway workers. The plan worked. Richard W. Sears turned a handsome profit, then moved to Minneapolis to establish the R.W. Sears Watch Company.

The following year, Sears moved to Chicago and partnered with Alvah C. Roebuck, a self-taught Hammond, Indiana, watchmaker he found through a Chicago Daily News classified ad. Roebuck soon asked Sears to buy him out, but not before lending his name to the company marquee: “Sears, Roebuck and Co.”

In 1888, Sears issued his first catalog, a thin mailer that featured only watches and jewelry. According to his apocryphal ad copy, which he always wrote himself, Sears claimed “THE LOWEST PRICES ON EARTH.” A consummate huckster, he soon started selling sundry items: buggies, bicycles, firearms, baby carriages and more.

Sears’s mail-order catalog, or “Big Book” as it was later known, became the Amazon of the Victorian era (and beyond). Like Amazon, Sears was a crucial cog in the American wheel, a giant of its time. Over its century-plus span, the Big Book grew to well over 1,000 pages and sold more than 100,000 items, including tools, hardware, apparel, appliances, furniture, sporting goods, auto supplies, farm equipment and entertainment centers. After opening its first brick-and-mortar store in 1925, Sears rose as the nation’s largest retail chain, introducing in-house brands like DieHard, Kenmore and Craftsman. In 1973, the company’s headquarters, the Sears Tower, became the tallest building in the world.

But as the 20th century faded, so did Sears—its brick-and-mortar businesses were replaced, ironically, by companies like Amazon, a convenient mail-order enterprise. On January 25, 1993, Sears ceased production of its famous Big Book catalog. In 2009, its famous Chicago skyscraper was renamed the Willis Tower. And in 2018, the company declared bankruptcy.

Over its 105-year run, the catalog was a fixture in Americans’ homes…

Read on for heroin, homes, virility aids, brain pills, “blood builder,” arsenic complexion wafers, tombstones, guns… “Before Folding 30 Years Ago, the Sears Catalog Sold Some Surprising Products,” from @smithsonianmag.bsky.social.

See also: “The Rise and Fall of Sears.”

* Georgia politician Eugene Talmadge, elected Governor four times in the 1930s and 40s

###

As we reflect on retailing, we might recall that it was on this date in 1958 that The world’s first publicly marketed instant noodles, Chikin Ramen, are introduced by Taiwanese-Japanese businessman Momofuku Ando.

“Americans are getting stronger. Twenty years ago, it took two people to carry ten dollars’ worth of groceries. Today, a five-year-old can do it.”*…

Scheduling note: the press of travel and obligation will make it impossible for your correspondent to post for the next few days; regular service should resume on or about Friday the 11th…

Rising prices prompted many consumers to shift to lower-cost goods from premium brands. However, as Ana Elena Azpúrua reports, an analysis of millions of products by Alberto Cavallo shows how inflation hit budget products harder in many countries, a phenomenon called “cheapflation”…

Surging inflation drove many consumers to cheaper brands or lower-quality products, but new data suggests that switching might not have saved them as much as they might have expected.

During the most recent period of high inflation, prices of the least expensive products increased more than those of the costliest, according to an analysis of microdata from large retailers by Harvard Business School Professor Alberto Cavallo. In a forthcoming article in the Journal of Monetary Economics, Cavallo and coauthor Oleksiy Kryvtsov, senior research officer at the Bank of Canada, refer to this phenomenon as “cheapflation.”

In the United States, the prices of the cheapest food products climbed 30 percent between January 2020 and May 2024, outpacing the 22 percent increase of the fanciest foods.

Kryvtsov and Cavallo, the Thomas S. Murphy Professor of Business Administration, analyzed millions of products from more than 90 big retailers in 10 countries, including detailed price data for products within the same categories, something that’s been difficult to study. After creating indexes tied to pre-pandemic prices, the researchers concluded that “cheapflation” isn’t unique to the US…

… The price gap between cheap and expensive goods widened most as inflation was peaking, but the spread remained even as prices stabilized, eating away consumers’ potential savings.

“Prices for cheaper brands grew between 1.3 and 1.9 times faster than the prices of more expensive brands, and only when inflation surged, not before or after,” the researchers write.

Why? Cavallo and Kryvtsov find evidence of an increase in the relative demand for cheaper products, as consumers shifted their spending from high to low-priced varieties in an attempt to lower their grocery bills. They also point out other reasons, including targeted fiscal stimulus, which likely increased the demand for cheaper varieties, and the possibility that cheaper products tend to depend more on global supply chains, like the ones disrupted by COVID-19. At the same time, the profit margins of cheaper goods could be tighter than those of makers of high-priced goods from the same category, adding pressure to raise prices as supply costs increased.

But when inflation decreased, “the relative prices of cheaper options remained permanently higher, even though the inflation inequality abated. This may help explain why some consumers may think that prices are ‘too high’: not just relative to the past, but also relative to more expensive varieties,” the authors write…

One reason we’re feeling the pinch: “Charting ‘Cheapflation’: How Budget Brands Got So Pricey,” @anaeazpurua on @albertocavallo in @HBSWK.

* Henny Youngman

###

As we scrimp, we might send developed birthday greetings to Jakaya Kikwete; he was born on this date in 1950. And economist and politician, he served as finance minister then President of Tanzania. Kikwete was instrumental in the political and economic reforms that have led to Tanzania being called “a success story” and served as chairperson of the African Union (in 2008–2009) and the chairman of the Southern African Development Community Troika on Peace, Defence and Security (in 2012–2013).

Since stepping down as President in 1915, Kikwete served as the African Union High Representative in Libya and as a member of the UN’s Lead Group of the Scaling Up Nutrition Movement. Since 2022, he has been a co-chairing the Commission for Universal Health convened by Chatham House, alongside Helen Clark.

“It’s easier to imagine the end of the world than the end of capitalism”*…

… so it’s useful to contemplate its beginning. David Rooney, in an excerpt from his book About Time…

Ömer Aga stood in the middle of Amsterdam’s Dam Square surrounded by his nineteen-strong party of advisers, interpreters and hosts, and gazed toward the huge new trading exchange that straddled the mighty Rokin canal, just to the south of the square. The year was 1614, and Aga was on a fact-finding mission to the Dutch Republic as the Ottoman Empire’s newest diplomatic emissary. Top of his list of must-see sights was this bold new building, completed just three years earlier. It was hard to miss, as it was the size of a soccer field and could accommodate thousands of traders in its 200-by-115-foot enclosed inner courtyard, but what Aga really noticed was the four-sided clock tower that loomed over the vast structure and the streets and canals all around, as well as the booming sound of its bell when they rang out the hours and then, at noon, tolled repeatedly for a few minutes before falling silent. Little did they realize it, but Omar Aga and his retinue were listening to one of the most significant clocks ever made. It was fitted to the world’s first stock exchange and sounded the birth of modern capitalism.

From the moment the Amsterdam exchange building first opened its doors in August 1611, traders were forbidden from trading anywhere else in the city. But the exchange did not just put spatial boundaries on trade. It concentrated traders in time, too. A few days before the new facility opened, the city council had issued a bylaw proclaiming that trading could only take place between the hours of 11 a.m. and noon, Monday to Saturday. At noon, the clock installed in the tower high above the exchange building would toll a bell for seven and a half minutes. If any traders were still in the exchange, or in the streets nearby, they would be fined. Additionally, trading was allowed between 6:30 p.m. and 7:30 p.m. during the summer months between May and August, and in winter evening trading took place for a thirty-minute period marked by a tolling bell at the city’s gates. At the end of evening trading, the exchange clock would again sound for seven and a half minutes and fines were issued for anyone caught trading after the bells fell silent.

Why were such strict limits placed on trading at the Amsterdam exchange? There were several reasons. One was a practical problem familiar to anybody involved with trade in a busy city center: time limits reduced congestion and disruption in the streets nearby. Another was that clocks made trading more efficient. Short, fixed trading hours concentrated buyers and sellers together, making it easier for each to find enough of the other. This increased the volume of trade, which was good for traders and for the city council collecting taxes on transactions. But clocks also helped prices to remain fair, as they could be used to regulate the people who occupied intermediate roles in the functioning of a market.

Some of the earliest references to mechanical clocks being used in towns and cities, in the Middle Ages and soon after, related to market restrictions. The first urban markets brought producers of food, cloth and so on into direct contact with the consumers of their wares. But as towns and cities grew, this model started to break down. It stopped making sense for every producer in the countryside to make the journey all the way to the center of towns. So, ‘intermediate trading’ emerged, whereby third parties might buy up the goods from several small producers somewhere on the edge of town, before bringing them in and selling them themselves at the market. Soon, a whole range of intermediate roles sprang up. Wholesalers, merchants, shopkeepers and peddlers were some, but intermediates also included financiers who advanced funds, and those speculating on the future in the hope of offsetting risk (whether because of bad harvests or other unpredictable events) and making more money. Some people occupied more than one role.

As populations grew and moved in increasing numbers to towns and cities, and markets began to sell more and more products, the rise of intermediate roles in market-based trade was inexorable, creating a new stratum of people who neither produced goods nor consumed them, but traded, speculated, brokered, hoarded, flipped and financed. Some market authorities feared intermediates would drive up prices or limit supplies and turned to clocks to control their involvement. Clocks meant that different groups could be treated differently at the market. In a sixteenth-century grain market, for instance, the first hours of trade could be restricted to residents, before bakers of bread could get in, and then the pastry bakers could enter. Only after several hours were wholesalers and other intermediate traders allowed in. But as societies and their market trading became ever more complex, the role of intermediates like brokers and financiers became increasingly important in keeping the flow of trading running smoothly. And, before long, finance became something that could be traded in its own right, and clocks took on a new regulatory role.

Amsterdam’s was not the first trading exchange. Antwerp and London had had exchanges since the sixteenth century where goods and money were traded, but Amsterdam was the first of a new kind of exchange: what became the modern securities exchange. As well as being a place to trade in commodities like salt or hides, people could also buy and sell financial assets. It started out as a place to buy and sell shares in the Dutch East India Company, an early joint-stock company and the first with freely tradable shares, but soon was used to trade other company shares, futures contracts and insurance policies as well as becoming the place to go for information about the state of the markets. The financial market had arrived, but its products, and the prices paid for them, which were time-dependent. The time at which each securities transaction was made, or would be enacted in the future, was central to this new type of trading to work fairly, everybody had to agree what time this was. In other words, trading needed time stamps, which is where the exchange clock came into its own. Clocks were no longer about excluding intermediates from the market. In the new exchanges, intermediates were the market — with the clock watching carefully over the whole thing…

The birth of modern capitalism and the role that timekeeping played in its nascence: The Amsterdam Stock Exchange, from @rooneyvision, via the invaluable @delanceyplace.

* Fredric Jameson (also sometimes attributed to Slavoj Žižek)

###

As we examine enterprise, we might recall that it was on this date in 1937 that Sylvan Goldman introduced the first shopping cart in his Humpty Dumpty grocery store in Oklahoma City.

“Those of us who read because we love it more than anything, feel about bookstores the way some people feel about jewelers”*…

Your correspondent is certainly among that number; bookstores– and libraries– are at the center of my mental map of civilization. So imagine my surprise when Alex Leslie delivered data demoting book shops in the literary hierarchy…

A lot of ink has been spilled over the decline of the dedicated bookstore – stores dedicated “just” or primarily to selling books – amid the rise of online retailers and e-readers in the 21st century. Yet dedicated bookstores were often not the main source of books in the U.S. historically. In fact, that market role was highly contested over the last two centuries.

In the early 20th century, a consumer could buy books from many different types of retailer. The specific focus, stock, clientele, and consumer experience of these different retailer types varied significantly and did much to shape the relationship between consumers (or readers) and books. In this richly varied market, the dedicated bookstore was outplayed on multiple fronts…

[Leslie brings the receipts…]

… Perhaps the most striking aspect of their position in the book retail market is how unstriking it is. Dedicated Bookstores represented a significant 7.5% of Lippincott’s revenue, yet they trailed behind News companies and Department Stores (Fig. 1). They carried less purchasing power at the individual level, where they fell in the middle of the pack behind less-common yet higher-volume retailer types like Foreign, Medical, and even Religious (Fig. 2). And while Bookstores were easily the second-most-common retailer of books, only 9% bought directly from Lippincott’s—meaning that they weren’t especially consistent either (Fig. 3).

Dedicated Bookstores were a major player in the book ecosystem, but they did not define it. They competed in a tight market where other retailer types beat them on affordability, breadth of location, specialized subject matter, and high-margin editions. In this context, dedicated Bookstores could all too easily become jacks of all trades and masters of none. A majority of Americans got their books from other retailers, and this was not entirely due to a lack of dedicated Bookstores in many towns: it also stemmed from a lack in dedicated Bookstores’ business model, a lack which continued to plague them into the 21st century even as they became more ubiquitous. For all our platitudes about the power of books writ large or reading as a single hobby, books seem to be less of a unifying force in their own right than the subjects they concern or the experiences they complement…

Still, I love them: “The Dedicated Bookstore Predicament,” from @azleslie.

* Anna Quindlen

###

As we browse, we might spare a thought for Count Lev Nikolayevich Tolstoy (known in English as Leo Tolstoy); he died on this date in 1910. A writer whose works adorn most bookstores, he is considered one of the greatest authors of all time. (He received nominations for the Nobel Prize in Literature every year from 1902 to 1906 and for the Nobel Peace Prize in 1901, 1902, and 1909, but never won. After one slight, August Strindberg and dozens of other authors and artists issued a proclamation shaming the Nobel Committee.)

Tolstoy is best known for War and Peace (1869) and Anna Karenina (1878), widely regarded as pinnacles of realistic fiction. In the late 1870s, after a profound moral crisis, followed by what he regarded as an equally profound spiritual awakening, he became a fervent Christian anarchist and pacifist. His ideas on nonviolent resistance, expressed in such works as The Kingdom of God Is Within You (1894), had a profound impact on such pivotal 20th-century figures as Mahatma Gandhi, Martin Luther King Jr., and Ludwig Wittgenstein.

“All we can do is stare at the pond, holding our breath”*…

Your correspondent is headed eight time zones away, so (Roughly) Daily will be on hiatus for a bit; regular service should resume on or about May 7.

In the meantime, enjoy Michael Turvey‘s (@tichaelmurvey) interactive “Koi Pond.”

* Haruki Murakami

###

As we contemplate, we might recall that it was on this date in 2003 that Apple launched iTunes. Downloading music had been already popularized by Napster, torrents, and others, but they operated largely outside the law, “sharing”; the sale of music was still confined largely to brick-and-mortar stores (and in a nascent way, to e-tailers like Amazon).

Steve Jobs approached Warner Music, Universal Music Group, and Sony Music to offer their music for 99 cents a song (and ten dollars for a full album). Their sales wounded by illegal file-sharing, the music labels were eager to staunch the bleeding; they struck the deal with Jobs.

iTunes was an instant success, selling over one million songs in its first week; it became the biggest music vendor in the U.S. five years later and remained a force for another decade or so… when it was overtaken by streaming.

You must be logged in to post a comment.