Posts Tagged ‘Henry George’

“An imbalance between rich and poor is the oldest and most fatal ailment of all republics”*…

Plutarch’s warning is one to take seriously–as then, now. So, how is the American Dream doing?…

In late 20th-century music, the elusiveness of the American Dream is a recurring theme. From Stevie Wonder’s ode to a boy “born in hard time Mississippi” in 1973 to Bruce Springsteen’s anthems to the working class in factory-shuttered towns in the 1980s, frustration with people’s inability to outgrow their circumstances is rife. The timing of the peak of that genre is no coincidence: whereas nearly all American children born in 1940 could still expect to do better than their parents, only two in five could by 1984…

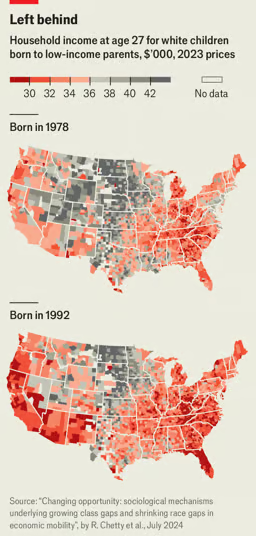

… A new study by Raj Chetty, of Harvard University, and colleagues provides fresh data on how America’s landscape of opportunity has shifted sharply over the past decades. Although at the national level there have been only small declines in mobility, the places and groups that have become more (or less) likely to enable children to rise up have changed a lot. The most striking finding is that, compared with the past, a child’s race is now less relevant for predicting their future and their socioeconomic class more so.

The greatest drops in mobility have been not in the places evoked in song, but on the coasts and the Great Plains, which historically provided pathways up (see maps). “Fifteen years ago, the American Dream was alive and well for white children born to low-income parents in much of the North-east and West Coast,” says Benjamin Goldman of Cornell University, one of the co-authors. “Now those areas have outcomes on par with Appalachia, the rustbelt and parts of the South-east.”

The fact that white children have become more likely to remain in poverty than before, whereas for black children the reverse is true, raises many questions. The finding comes from tracing the trajectories of 57m children born in America between 1978 and 1992 and looking at their outcomes by the age of 27. “This is really the first look with modern big data into how opportunity can change within a place over time,” says Mr Goldman. For children born into high-income families, household income increased for all races between birth cohorts. Yet among those from low-income families, earnings rose for black children and fell for white children.

A black child born to poor parents in 1992 earned $1,400 a year more than one born in 1978. A similar white child earned $2,000 less than one born in 1978. But on average, a poor white child still earned $9,500 more than a poor black child.

This pattern has played out in virtually every county, though with big regional differences. As a result, the earnings gap between rich and poor white children (the “class gap”) grew by 27%, whereas the earnings gap between poor white and poor black children (the “race gap”) fell by 28%…

… None of this means that race is no longer relevant for Americans’ chances in life. Although the reversal of the direction of travel is striking, a young black American born in 1992 to poor parents was still four percentage points more likely to remain in poverty than a poor white peer, down from a 15 percentage-point gap for those born in 1978. And while the near doubling in rates of mortality among young, lower-income white Americans is deeply alarming, mortality rates for their black counterparts have increased too, and they are still (a bit) more likely to die young…

… Convergence has not yet brought equality. Despite improvements across America for poor black children, there is still no county where their outcomes match those of poor white ones. Yet the decline of the white working class is steep, and bound to cause grief. Telling a young white man with lower life outcomes than previous generations that he is still doing better than the average black peer is about as useful as telling a young black man that he’s doing well “for a black man”.

Another possible misconception is that social mobility is a zero-sum game: that poor white children are doing worse because poor black children are doing better. The authors tackle this by showing how in places where black children have done well, white children’s outcomes have remained stable; and in places where white children have done particularly poorly, their black peers have also not thrived.

In his previous work Mr Chetty demonstrated [see here for a summary of his 2018 study] just how much a child’s chances of outperforming their parents depended on their race and where they grew up. One of the questions the authors were left with was how “sticky” these effects would be over time: could opportunities for the next cohorts of children change within these same places, or were they fixed? The new study’s most hopeful finding is that, far from being fixed, opportunities within a place can change significantly and rapidly. Neither history nor place is destiny…

… Americans love a rags-to-riches story. In his acceptance speech [at the Republican Convention], Mr Vance pledged to “make this country a place where every dream…will be possible once again”. In his bestselling book “Hillbilly Elegy” he writes that the assumption “that only a truly extraordinary person could have made it to where I am today…I think that theory is a load of bullshit.”

But the story of Mr. Vance, who grew up in a poor part of the rustbelt, rose to be a venture capitalist and now, at 39, is a potential American president, remains extraordinarily rare. While there has been a reshuffling of opportunities for Americans trying to escape the lowest rung, there has been no progress at all for routes into the upper class. For the vast majority of poor black children, who continue to have a 3% chance of rising from the bottom to the top quintile, and poor white children, whose chances have fallen from 14% to 12%, that door remains firmly shut…

“Class, race and the chances of outgrowing poverty in America,” a big-data analysis– a gift article from @TheEconomist.

* Plutarch

###

As we optimize opportunity, we might send mortgaged birthday greetings to Charles Darrow; he was born on this date in 1889. He designed (in 1933) and patented (in 1935) the board game Monopoly. He later sold his patent to Parker Brothers, which credits him as its creator.

In fact, the history of Monopoly is much longer. It can be traced back to 1903, when American anti-monopolist Lizzie Magie created a game called The Landlord’s Game that she hoped would explain the single-tax theory of Henry George. It was intended as an educational tool to illustrate the negative consequences of concentrating land in private monopolies.

After losing his job at a sales company following the Stock Market Crash of 1929, Darrow worked at various odd jobs. Seeing his neighbors and acquaintances play a board game in which the object was to buy and sell property, he decided to publish his own version of the game.

In fact, Darrow and his friends were just a few of many people in the American Midwest and East Coast who had been playing a game of buying and trading property– all based on Magie’s original… but most having morphed as warnings of that sort too often do) into the opposite of Magie’s intent– a celebration of accumulation. The game was used by college professors and their students, and another variant, called The Fascinating Game of Finance, was published in the Midwest in 1932. From there the game traveled back east, where it had remained popular in Pennsylvania, and became popular with a group of Quakers in Atlantic City. Darrow was taught to play the game by Charles Todd, who had played it in Atlantic City, where it had been customized with that city’s street and property names– to wit Monopoly‘s nomenclature.

“The solution to poverty is to abolish it directly”*…

The idea of a guaranteed flow of funds to allow anyone and everyone to meet basic needs– as we’re currently discussing it, a universal basic income– has been getting significant attention in recent decades. But as Karl Widerquist explains (in an excerpt from his recent book, Universal Basic Income). “UBI” dates back as a concept– and as a practice– many centuries…

Support for Universal Basic Income (UBI) has grown so rapidly over the past few years that people might think the idea appeared out of nowhere. In fact, the idea has roots going back hundreds or even thousands of years, and activists have been floating similar ideas with gradually increasing frequency for more than a century.

Since 1900, the concept of a basic income guarantee (BIG) has experienced three distinct waves of support, each larger than the last. The first, from 1910 to 1940, was followed by a down period in the 1940s and 1950s. A second and larger wave of support happened in the 1960s and 1970s, followed by another lull in most countries through about 2010. BIG’s third, most international, and by far largest wave of support began to take off in the early 2010s, and it has increased every year since then.

[But] We could trace the beginnings of UBI into prehistory, because many have observed that “prehistoric” (in the sense of nonliterate) societies had two ways of doing things that might be considered forms of unconditional income…

From pre-historic nomads, through ancient Athens, to Thomas Paine and then Henry George, Widerquist unspools the history of UBI, then walks through the “three waves” that began in the early 20th century, concluding with the current state of the debate: “The Deep and Enduring History of Universal Basic Income,” from @KarlWiderquist and @mitpress.

For more on the recent history of the UBI debate, see Widerquist’s essay, “Three Waves of Basic Income Support.”

And for a peak at the results of (small, incomplete, but encouraging) experiments in this direction, see: “Places across the U.S. are testing no-strings cash as part of the social safety net,” from @NPR.

* Dr. Martin Luther King, Jr.

###

As we ponder poverty, we might send thoughtful birthday greeting to James Tobin; he was born on this date in 1918. An economist who contributed to the development of key ideas in the Keynesian economics of his generation, he made pioneering contributions to the study of investment, monetary and fiscal policy, and financial markets– for which he shared the Nobel Memorial Prize in Economic Sciences in 1981.

Outside academia, Tobin is probably best known for his suggestion of a tax on foreign exchange transactions, now known as the “Tobin tax,” designed to reduce speculation in the international currency markets, which he saw as dangerous and unproductive.

And relevantly to the piece above, Tobin, Paul Samuelson, John Kenneth Galbraith and another 1,200 economists signed a document in 1968 calling for the U. S. Congress to introduce that year a system of income guarantees and supplements– a UBI.

“The malady of commercial crisis is not, in essence, a matter of the purse but of the mind”*…

Still, those crises do take tangible form…

Q3 is a traditional peak season in the world of shipping, but not this year. Global inflation, weakened consumer demand and excess cargo carrying capacity are pushing the market down…

With a gloomy economic outlook and vague alarms from central banks, it seems recession could be just around the corner.

Are there any indications from the shipping market when global recession is on its way? This is a question not only of interest to the commercial and technical players in the maritime industry, but also to financiers and policy makers.

The last recession triggered by economic factors was the Great Recession from December 2007 to June 2009. Goods loaded worldwide for seaborne trade fell by nearly five percent in 2009 compared to 2008, from about 8.23 billion tons to 7.82, according to UNCTAD’s Handbook of Statistics 2021.

Is a depressed shipping market a contributor to global recession, or does global recession lead the shipping market down? It is a chicken and egg question. But can the Great Recession’s impact to shipping market provide some useful reference to the current situation? Shipping indexes may shed some light.

…

How is the shipping market now? In May 2022, bulker earnings started to drop. Tankers were at a short break in an upward rise. Container freight rates were flat and just about to begin sliding. As of September 2022, only tankers’ earnings are still climbing.

The bulk shipping market’s underperformance will probably continue and will not turn before Christmas, unless there are significant changes – for example, if an easing of COVID restrictions in China pushes up its industrial demand (particularly for iron ore). Demand for oil and gas from the West will help send tanker rates continue soaring. Container shipping is expected to decline in the short term.

During the past months, a black cloud has appeared on the global shipping market’s horizon. The downward trend of shipping indexes brings a sense of foreboding. As to the question, “is a global recession imminent?” Most likely, say signals from these two shipping indexes…

“Do Shipping Indexes Hint at Global Recession?,” from @Mar_Ex. (TotH to friend PH.)

See also: “China lockdowns accelerate supply chain diversion and box shipping review,” and more generally, “An often-overlooked economic measure is signaling serious trouble ahead” and “Three Harbingers Point to a U.S. Recession.”

* John Stuart Mill

###

As we batten the hatches, we might we might spare a thought for Henry George; he died on this date in 1897. A writer, politician and political economist, George is best remembered for Progress and Poverty, published in 1879, which treats inequality and the cyclic nature of industrialized economies, and proposes the use of a land value tax (AKA a “single tax” on real estate) as a remedy– an economic philosophy known as Georgism, the main tenet of which is that, while individuals should own what they create, everything found in nature, most importantly the value of land, belongs equally to all mankind.

George’s ideas were widely-discussed in his time and into the early 20th century, and admired by thinkers like Alfred Russel Wallace, Jose Marti, and William Jennings Bryan; Franklin D. Roosevelt sang his praises, as did George Bernard Shaw. But with the rise of neoclassical economics, George’s star began to recede. Still, more modern thinkers like Albert Einstein and martin Luther King were fans.

In a sequence that mimicked George’s arc of influence, it was George’s work that inspired Elizabeth Magie to create The Landlord’s Game in 1904 to demonstrate his theories; ironically, it was Magie’s board game that became in the 1930s (as recently noted here and here) the basis for Monopoly.

In 1977, Joseph Stiglitz showed that under certain conditions, spending by the government on public goods will increase aggregate land rents/returns by the same amount. Stiglitz’s findings were dubbed “the Henry George Theorem,” as they illustrate a situation in which Henry George’s “single tax” is not only efficient, it is the only tax necessary to finance public expenditures.

“Man is the only animal whose desires increase as they are fed; the only animal that is never satisfied.”*…

(Roughly) Daily readers have encountered Henry George here before. An economist who wrote late in the 19th century, he was hugely influential in his time and into the early 20th century. Indeed, his philosophy was the inspiration for (original) version of the game Monopoly. Michael Kinsley argues that we should take another look…

So, you’re a Silicon Valley billionaire and you’ve already got the private plane. What you need next is a philosophy, something to live by, and to help finance, and—most important—to use to explain or justify yourself. Don’t just grab the next philosophy to come along. Chances are that will be Ayn Rand and her extreme form of capitalism, which she called objectivism.

Rand has a lot going for her, to be sure. First, you may have actually read her in high school and may have been genuinely influenced. Second, in a nutshell, she rationalizes greed, which you have nothing against. Third, she was into mildly kinky sex—something else you may have in common. Fourth, she was associated in some way you don’t quite follow with Alan Greenspan, who is respectability itself, whatever other Rand enthusiasts may have been up to.

But you’re too late. Ayn Rand, who never was really undiscovered (The Fountainhead became a movie, starring Gary Cooper as a heroic architect, a few years after it was published), has by now been thoroughly re-discovered. According to James Stewart (the prominent business journalist, not the even more prominent actor), writing in The New York Times, President Trump says Ayn Rand is his favorite writer and that The Fountainhead, her pulmonary embolism of a book, is his favorite novel. Travis Kalanick, the onetime Übermensch of Uber, is on board, as is (liberal foodies, please note) John Mackey, co-founder and C.E.O. of Whole Foods.

My dear billionaire, you need an economist almost no one has heard of. One who addressed the most pressing problems of today, which do not include the insufficient greed of rich people. But one who was not completely out of sympathy with rich people, either.

May I nominate Henry George (1839–97)—economist, pamphleteer, journalist? Once famous, he is now widely forgotten. He described himself as a man who came out of the great American West, which he did—but only after he got there via Philadelphia, where he was born. He later moved to New York City, ran for mayor, and attracted 10,000 people to a political rally (but lost nonetheless). He made the best-ever short defense of free trade: You wouldn’t fill your harbor with rocks to keep out goods your citizens want to buy, would you? Well, that’s what you’re doing when you slap tariffs on imports.

George’s masterwork, published in 1879, was Progress and Poverty, which set forth to explain how “increase of want” could go hand in hand with “increase of wealth.” Thus George took on precisely the question we face today: not the general question of poverty or inequity, but why specifically are middle-class incomes stagnating, and incomes of people at the bottom falling, while those at the top continue to rise?

George was no vulgar Marxist. You might call him a “supply-side socialist.” All products of the economy, he reasoned, are ultimately derived from three sources: labor, capital, and land. What else is there? Labor and capital are both productive. Put them to work and you end up with more. But land is different. As the man said, “They aren’t making any more of it.” When you work for an hour, you increase society’s wealth (and your own) by an hour’s worth of wages. When you save a dollar rather than spending it, you increase society’s (and your own) wealth by a dollar. But when you buy a piece of land for $10,000 and sell it for $20,000, you haven’t increased the total wealth of society by a nickel. Yet the price of land keeps going up, up, up, as the population increases and society grows richer. Where does that money come from? It comes from the pockets of the other two factors of production, labor and capital.

George distinguished, in other words, between the capitalist who is truly productive and the capitalist who is simply a “landlord.”… You’ve got to think of “land” as a metaphor for all unproductive forms of capitalism. Much of the financial industry, for example: hedge funds, private equity, I.P.O.’s and I.R.A.’s. Some might defend finance as an industry that makes the making of what other industries make more efficient. But when you read that Goldman Sachs is getting some enormous fee for fuck-all or that two companies are merging that unmerged a few years ago and will unmerge again in a few years, you gotta wonder…

Henry George’s theories might have something to offer people who want to put their money to good use today: “The Obscure Economist Silicon Valley Billionaires Should Dump Ayn Rand For,” from @michaelkinsley in @VanityFair. Eminently worth reading in full and pondering.

* Henry George (who, to Kinsley’s observation that he might be considered a “supply-side socialist,” also said: “Laissez faire (in its full true meaning) opens the way to the realization of the noble dreams of socialism.”

###

As we return to first principles, we might recall that it was on this date in 1996 that Oprah Winfrey launched Oprah’s Book Club (with he then recently published novel The Deep End of the Ocean by Jacquelyn Mitchard). In total the club recommended 70 books during its 15 years in its original (Oprah Winfrey Show form), and has subsequently been revived via OWN: The Oprah Winfrey Network, O, The Oprah Magazine, and Apple TV.

While the selections have occasionally generated some controversy (e.g., Michale Franzen, James Frey), they have for the most part been warmly– and enthusiastically– received, adding massive sales to the chosen titles. Indeed (per Business Week), publishers estimate that her power to sell a book is anywhere from 20 to 100 times that of any other media personality.

This year, Oprah was awarded the PEN/Faulkner Literary Champion award, which “recognizes a lifetime of devoted literary advocacy and a commitment to inspiring new generations of readers and writers.”

“An imbalance between rich and poor is the oldest and most fatal ailment of all republics”*…

In a stark sign of the economic inequality that has marked the pandemic recession and recovery, Americans as a whole are now earning the same amount in wages and salaries that they did before the virus struck — even with nearly 9 million fewer people working.

The turnaround in total wages underscores how disproportionately America’s job losses have afflicted workers in lower-income occupations rather than in higher-paying industries, where employees have actually gained jobs as well as income since early last year.

In February 2020, Americans earned $9.66 trillion in wages and salaries, at a seasonally adjusted annual rate, according to the Commerce Department data. By April, after the virus had flattened the U.S. economy, that figure had shrunk by 10%. It then gradually recovered before reaching $9.67 trillion in December, the latest period for which data is available.

Those dollar figures include only wages and salaries that people earned from jobs. They don’t include money that tens of millions of Americans have received from unemployment benefits or the Social Security and other aid that goes to many other households. The figures also don’t include investment income…

The figures document that the vanished earnings from 8.9 million Americans who have lost jobs to the pandemic remain less than the combined salaries of new hires and the pay raises that the 150 million Americans who have kept their jobs have received.

The job cuts resulting from the pandemic recession have fallen heavily on lower-income workers across the service sector— from restaurants and hotels to retail stores and entertainment venues. By contrast, tens of millions of higher-income Americans, especially those able to work from home, have managed to keep or acquire jobs and continue to receive pay increases.

“We’ve never seen anything like that before,” said Richard Deitz, a senior economist at the Federal Reserve Bank of New York, referring to the concentration of job losses. “It’s a totally different kind of downturn than we’ve experienced in modern times.”

The figures also underscore the unusually accelerated nature of this recession. As a whole, both the job losses that struck early last spring and the initial rebound in hiring that followed have happened much faster than they did in previous recessions and recoveries. After the Great Recession, for example, it took nearly 2 1/2 years for wages and salaries to regain their pre-recession levels…

One reason why the job losses have had relatively little impact on the nation’s total pay is that so many of the affected employees worked part time. The average work week in the industry that includes hotels, restaurants and bars is just below 26 hours. That’s the shortest such figure among 13 major industries tracked by the government. The next shortest is retail, at about 31 hours. The average for all industries is nearly 35 hours.

The recovery in wages and salaries helps explain why some states haven’t suffered as sharp a drop in tax revenue as many had feared. That is especially true for states that rely on progressive taxes that fall more heavily on the rich. California, for example, said last month that it has a $15 billion budget surplus. Yet many cities are still struggling, and local transit agencies, such as New York City’s subway, have been hammered by the pandemic.

The wage and salary data also helps explain the steady gains in the stock market, which have been led by high-tech companies whose products are being heavily purchased and used by higher-income Americans, such as Apple iPads, Peloton bikes, or Amazon’s online shopping.

This week, the New York Fed released research that underscored how focused the job losses have been. For people making less than $30,000 a year, employment has fallen 14% as of December. For those earning more than $85,000, it has actually risen slightly. For those in-between, employment has fallen 4%…

Some companies have cut wages in this recession, but on the whole the many millions of Americans fortunate enough to keep their jobs have generally received pay raises at largely pre-recession rates. Some of those income gains likely reflect cost-of-living raises; the Commerce Department’s wage and salary data isn’t adjusted for inflation…

Truman Bewley, a retired Yale University economist who wrote a book about the concept of sticky wages, said that most companies have a key core of workers they rely on through hard times and are reluctant to cut pay for them.

And there’s another reason, Bewley said, why many companies cut jobs instead of pay. While researching his book, he said a factory manager told him why his company did so: “It gets the misery out the door.”

More at: “Sign of inequality: US salaries recover even as jobs haven’t.”

See also “More Than 33 Million Americans Have Filed for Unemployment During Coronavirus Pandemic.” source of the image above.

And to compare the U.S. to other countries, try this nifty interactive visualization.

* Plutarch

###

As we examine equity, we might send foundational birthday greetings to Pierre le Pesant, sieur de Boisguilbert; he was born on this date in 1646. A French lawmaker and a Jansenist, he is best remembered as one of the inventors of the notion of an economic market– he championed free trade in opposition to Colbert‘s mercantilist views (which generated government revenues through duties and tariffs).

But he is also noteworthy as the champion of a single tax on each citizen (in lieu of all tariffs, customs, and other trade-related fees) that in some ways presaged Henry George‘s proposals.

You must be logged in to post a comment.