Posts Tagged ‘inflation’

“Inequality is as dear to the American heart as liberty itself”*…

And indeed, what was true a century ago seem still to hold. Everyone seems to hate/fear inflation, but it has radically different impacts on different groups within our society…

Inflation is widening America’s wealth gap.

• Prices have risen across the nation, and so have wages across all income levels.

• The lowest-earning households gained an average of $500 in earnings last year. But their expenses grew by almost $2,000.

• Meanwhile, the upper half of earners pulled further ahead as their incomes outgrew expenses significantly.

“Whom does inflation hurt the most?” from Scott Galloway (@profgalloway)

###

As we ferret out unfairness, we might cautious birthday greetings to James Mill; he was born (James Milne) on this date in 1773. A historian, economist, political theorist, and philosopher (a close ally of Utilitarian thinker Jeremy Bentham), he is counted among the founders of the Ricardian school of economics (and so, among other things, a father of monetarism, the theory that excess currency leads to inflation).

His son, John Stuart Mill, studied with both Bentham and his father, then became one of most influential thinkers in the history of classical liberalism (perhaps especially his definition of liberty as justifying the freedom of the individual in opposition to unlimited state and social control). JSM also followed his father in justifying colonialism on Utilitarian lines, and served as a colonial administrator at the East India Company.

“We do not inherit the earth from our ancestors, we borrow it from our children”*…

… and the interest rate on that loan is rising.

There’s much discussion of what’s causing the sudden-feeling spike in prices that we’re experiencing: pandemic disruptions, nativist and protectionist policies, the over-taxing of over-optimized supply chains, and others. But Robinson Meyer argues that there’s another issue, an underlying cause, that’s not getting the attention it deserves… one that will likely be even harder to address…

Over the past year, U.S. consumer prices have risen 7 percent, their fastest rate in nearly four decades, frustrating households and tanking President Joe Biden’s approval rating. And no wonder. High inflation corrodes the basic machinery of the economy, unsettling consumers, troubling companies, and preventing everyone from making sturdy plans for the future…

For years, scientists and economists have warned that climate change could cause massive shortages of major commodities, such as wine, chocolate, and cereals. Financial regulators have cautioned against a “disorderly transition,” in which the world commits only haphazardly to leaving fossil fuels, so it does not invest enough in their zero-carbon replacements. In an economy as prosperous and powerful as America’s, those problems are likely to show up—at least at first—not as empty grocery shelves or bankrupt gas stations but as price increases.

That phenomenon, long hypothesized, may be starting to actually arrive. Over the past year, unprecedented weather disasters have caused the price of key commodities to spike, and a volatile oil-and-gas market has allowed Russia and Saudi Arabia to exert geopolitical force.

“This climate-change risk to the supply chain—it’s actually real. It is happening now,” Mohamed Kande, the U.S. and global advisory leader at the accounting firm PwC, told me.

…

How to respond to these problems? The U.S. government has one tool to slow down the great chase of inflation: Leash up its dollars. By raising the rate at which the federal government lends money to banks, the Federal Reserve makes it more expensive for businesses or consumers to take out loans themselves. This brings demand in the economy more in line with supply. It is like the king in our thought experiment deciding to buy back some of his gold coins.

But wait—is it always appropriate to focus on dollars? What if the problem was caused by too few goods? Worse, what if the economy lost the ability to produce goods over time, throwing off the dollars-to-goods ratio? Then what was once an adequate number of dollars will, through no fault of its own, become too many...

… if the climate scars on supply continue to grow, does the Federal Reserve have the right tools to manage? Stinson Dean, the lumber trader, is doubtful. “Raising interest rates will blunt demand for housing—no doubt. But if you blunt demand enough to bring lumber prices down, you’re destroying the economy,” Dean told me. “For us to have lower lumber prices, we can only build a million homes a year. Do you really want to do that?

“Raising rates,” he said, “doesn’t grow more trees.” Nor does it grow more coffee, end a drought, or bring certainty to the energy transition. And if our new era of climate-driven inflation takes hold, America will need more than higher interest rates to bring balance to supply and demand.

A provocative look at the tangled roots of our inflation, suggesting that “The World Isn’t Ready for Climate-Change-Driven Inflation,” from @yayitsrob in @TheAtlantic. Eminently worth reading in full. Via @sentiers.

* Native American proverb

###

As we dig deeper, we might send carefully calculated birthday greetings to Frank Plumpton Ramsey; he was born on this date in 1903. A philosopher, mathematician, and economist, he made major contributions to all three fields before his death (at the age of 26) on this date in 1930.

While he is probably best remembered as a mathematician and logician and as Wittgenstein’s friend and translator, he wrote three paper in economics: on subjective probability and utility (a response to Keynes, 1926), on optimal taxation (1927, described by Joseph E. Stiglitz as “a landmark in the economics of public finance”), and optimal economic growth (1928; hailed by Keynes as “”one of the most remarkable contributions to mathematical economics ever made”). The economist Paul Samuelson described them in 1970 as “three great legacies – legacies that were for the most part mere by-products of his major interest in the foundations of mathematics and knowledge.”

For more on Ramsey and his thought, see “One of the Great Intellects of His Time,” “The Man Who Thought Too Fast,” and Ramsey’s entry in the Stanford Encyclopedia of Philosophy.

“Anyone who lives within their means suffers from a lack of imagination”*…

A remarkable true tale from the always-illuminating folks at Planet Money…

This is a story about how an economist and his buddies tricked the people of Brazil into saving the country from rampant inflation. They had a crazy, unlikely plan, and it worked.

Twenty years ago, Brazil’s inflation rate hit 80 percent per month. At that rate, if eggs cost $1 one day, they’ll cost $2 a month later. If it keeps up for a year, they’ll cost $1,000…

“How Fake Money Saved Brazil,” from @planetmoney and @NPR.

For an even more complete telling, listen to the podcast: “How Four Drinking Buddies Saved Brazil.”

* Oscar Wilde

###

As we follow the money, we might recall that it was on this date in 1941, in his State of the Union Address, the president Franklin D. Roosevelt outlined the Four Freedoms— the fundamental values of democracy: freedom of speech, freedom of worship, freedom from want, freedom from fear. These precepts were furthered by Eleanor Roosevelt, who incorporated them into the Preamble to the United Nations Universal Declaration of Human Rights.

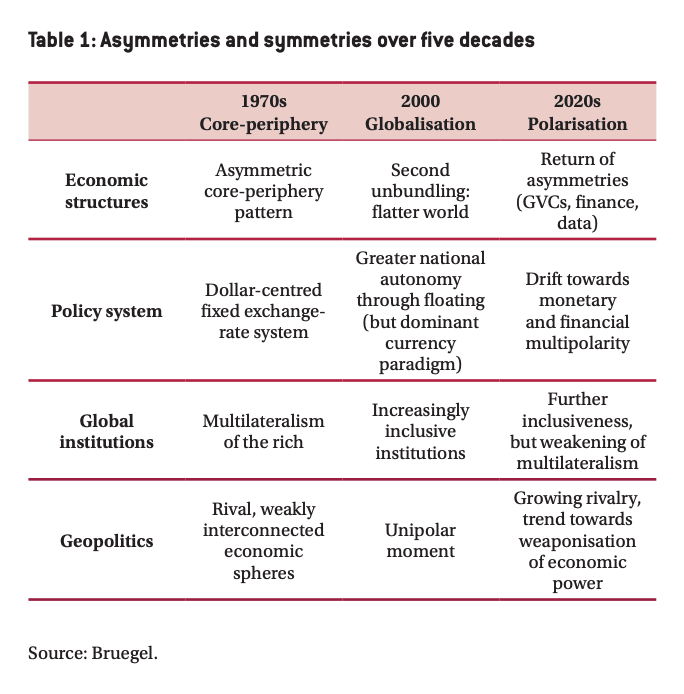

“Symmetry is not the way of the world in all times and places”*…

What a difference a couple of decades make…

Asymmetries are back. Rising market power, the sudden ubiquity of global digital networks, hierarchical hub-and-spoke structures in international trade and finance and the enduring dominance of the US dollar, despite the transition to floating exchange rates, all point to their resurgence. The remarkable decay of economic multilateralism in the very fields – trade and development finance – where global rules and institutions were first tried and reigned supreme for decades, is paving the way to a redefinition of international relations on a bilateral or regional basis, with powerful countries setting their own rules of the game. This transformation is compounded by the strengthening of geopolitical rivalry between the US, China and a handful of second-tier powers.

Donald Trump’s attempt to leverage US centrality in the global economy to extract rents from economic partners was short-lived. But US policy has certainly changed permanently. For all its friendly intentions, the Biden administration leaves no doubt about its overriding priorities: a foreign policy for the (domestic) middle class – to quote the title of a recent report (Ahmed et al, 2020) – and the preservation of the US edge over China. China, for its part, has set itself the goal of becoming by 2049 a “fully developed, rich and power-ful” nation and does not show any intention to play by multi-lateral rules that were conceived by others. In this context, the rapid escalation of great power competition between Washington and Beijing is driving both rivals towards the building of competing systems of bilateral or regional arrangements.

What is emerging is not only an asymmetric hub-and-spoke landscape. It is a world in which hubs are controlled by major geopolitical powers – in other words, a multipolar, fragmented world. Nothing indicates that these asymmetries will fade away any time soon. On the contrary, economic, systemic and geopolitical factors all suggest they may prove persistent. We will have to learn to live with them.

There are several consequences. First, this new context calls for an analytical reassessment. Recent research has put the spotlight on a series of economic, financial or monetary asymmetries and has begun to uncover their determinants and effects. Analytical and empirical tools are available that make it possible to gather systematic evidence and to document the impact of asymmetries on the distribution of the gains from economic interdependence. We are on our way to learning more about the welfare and the policy implications of participating in an increasingly asymmetric global system.

Second, the relationship between economics and geopolitics must now be looked at in a more systematic way. For many years – even before the demise of the Soviet Union – international economic relations were considered in isolation, at least by economists. They were looked at as if they were (mostly) immune from geopolitical tensions. This stance is no longer tenable, at a time when great-power rivalry is reasserting itself as a key determinant of policy decisions. Whatever their wishes, economists have no choice but to respond to this new reality. They should document the potential for coercion by powers in control of crucial nodes or infrastructures and the risks involved in participating in the global economy from a vulnerable position.

Third, supporters of multilateralism need to wake up to the new context. They have too often championed a world made up of peaceful and balanced relations that bears limited resemblance to reality. Because power and asymmetry can only be forgotten at one’s own risk, neglecting them inevitably fuels mistrust of principles, rules and institutions that are perceived as biased. Multilateralism remains essential, but institutions are not immune to the risk of capture.

Asymmetry, however, does not imply a change of paradigm. Even if it affects the distribution of gains from trade, it does not abolish them. And in a world in which global public goods (and bads) have moved to the forefront of the policy agenda, there is no alternative to cooperation and institutionalised collective action. The prevention of climate-related disasters, maintenance of public health and preservation of biodiversity will remain vital tasks whatever the state of inter-national relations. What asymmetries call for is an adaptation of policy template. The multilateral project should not be ditched, but it must be rooted in reality.

Understanding the emerging new global economy: from the conclusion of Jean Pisani-Ferry‘s (@pisaniferry) paper, “Global Assymetries Strike Back,” eminently worth reading in full. [Via @adam_tooze]

* Charles Kindelberger, economic historian and architect of the Marshall Plan

###

As we find our place, we might send tight birthday greetings to Paul Adolph Volcker Jr.; he was born on this date in 1927. An economist, he was appointed Federal Reserve Chair by President Carter in 1979, and reappointed by President Reagan. He took that office in a time of “stagflation” in the U.S.; his tight money policies, combined with Reagan’s expansive fiscal policy(large tax cuts and a major increase in military spending), tamed inflation, but led to much larger federal deficits (and thus, higher federal interest costs) and increased economic imbalances across the economy. In the end, Reagan let Volcker go; as Joseph Stiglitz observed, “Paul Volcker… known for keeping inflation under control, was fired because the Reagan administration didn’t believe he was an adequate de-regulator.”

Volcker returned to government service in 2009 as the chairman of President Obama’s Economic Recovery Advisory Board. In 2010, Obama proposed bank regulations which he dubbed “The Volcker Rule,” which would prevent commercial banks from owning and investing in hedge funds and private equity, and limit the trading they do for their own accounts (a reprise of a key element in the then-defunct Glass-Steagell Act). It was enacted; but in 2020, FDIC officials said the agency would loosen the restrictions of the Volcker Rule, allowing banks to more easily make large investments into venture capital and similar funds.

“What is it that happens in an inflation? The unit of money suddenly loses its identity.”*…

Today the Bureau of Labor Statistics releases its Consumer Price Index for the month of March. Here is some important context to help understand the figures…

When inflation numbers come out on April 13, they will likely look very high. And measured annually, inflation will probably rise further over the next few months. These headline numbers will be used to argue against the American Jobs Plan and future infrastructure investments, and even to advocate austerity.

But this response will be wrong, for three reasons:

1) The high year-over-year inflation of the coming months will reflect the falling prices of a year ago, whether or not prices are rising more rapidly today.

2) Achieving the Federal Reserve’s price-stability goals requires a period of above-trend inflation; if inflation, correctly measured, rises modestly in the coming months, that’s a good thing.

3) Even if inflation is a genuine problem, scaling back infrastructure investment is not the solution. It might even make the problem worse…

The full explanation at “The Illusion of Inflation: Why This Spring’s Numbers Will Look Artificially High.”

(Image above: source)

* Elias Canetti, Crowds and Power

###

As we steel ourselves, we might spare a thought for James Buchanan “Diamond Jim” Brady; he died on this date in 1917. A businessman and celebrity in the Gilded Age, he made his fortune semi-scrupulously in the rail industry and less scrupulously in stock trading and fixed bets.

His appetites for indulgences of all sorts were legendarily huge; but his nickname was a nod to the main among them– to his obsession with jewels, especially diamonds. He amassed stones worth $2 million (equivalent to approximately $61,464,000 in 2019 dollars).

You must be logged in to post a comment.