Posts Tagged ‘Federal Reserve’

“You get what you measure”*…

Matt Stoller takes the occasion of Trump’s selection of Kevin Warsh to head the Fed (“an orthodox Wall Street GOP pick, though he is married to the billionaire heiress of the Estee Lauder fortune and was named in the Epstein files. He’s perceived not as a Trump loyalist but as an avatar of capital”) to ponder why public satisfaction with the economy is so low (“if you judge solely by consumer sentiment, Trump’s first term was the third best economy Americans experienced since 1960. Trump’s second term is not only worse than his first, it is the worst economic management ever recorded by this indicator”).

Stoller argues that we’re mesuring the wrong things (or, in some cases, the right things in the wrong ways)…

… the models underpinning how policymakers think about the economy just don’t reflect the realities of modern commerce. The fundamental dynamic is that those models were constructed in an era where America was one discrete economy, with Wall Street and the public tied together by the housing finance system. But today, Americans increasingly live in tiered bubbles that have less and less to do with one another. Warsh will essentially be looking at the wrong indicators, pushing buttons that are mislabeled.

While corporate America is experiencing good times, much of the country is experiencing recessionary conditions. Let’s contrast consumer sentiment indicators with statistics showing an economic boom. Last week, the government came out with stats on real gross domestic product increasing at a scorching 4.4% in the third quarter of last year. There’s higher consumer spending, corporate investment, government spending, and a better trade balance. Inflation, according to the Consumer Price Index, is low at 2.6.% over the past year. And while official numbers aren’t out for the final three months of the year, the Atlanta Fed’s GDPNow forecast shows that it estimates growth at 4.2%. And there are other indicators showing prosperity, from low unemployment to high business formation, which was up about 8% last year, as well as record corporate profits…

… Behavioral economists and psychologists have all sorts of reasons to explain that people don’t really understand the economy particularly well. But in general, when the stats and the public mood conflict, I believe the public is usually correct. Often, there are some weird anomalies with the data used by policymakers. In 2023, I noticed that the consumer price index, the typical measure of inflation, didn’t account for borrowing costs, so the Fed hike cycle, which caused increases in credit card, mortgage, auto loan, payday loans, et al, just wasn’t incorporated. The public wasn’t mad at phantom inflation, they were mad at real inflation that the “experts” didn’t see.

I don’t think that’s the only miscalculation…

[Stoller goes on to explain the ways in which “consumer spending” doesn’t tell us much about consumers anymore, about the painful reality of “spending inequality,” and about the obscure(d) problem of monopoly-driven inflation. He concludes…]

… Finally, there’s a more philosophical point, which I don’t think explains the short-term frustrations people feel, but is directionally correct. Do people actually want what the economy is producing? For most of the 20th century, the answer was yes. When Simon Kuznets invented these measurement statistics in 1934, financial value and the value that Americans placed on products and services were similar. A bigger economy meant things like toilets and electricity spreading across rural America, and cars and food and washing machines.

Today? Well, that’s less clear. According to the Bureau of Labor Statistics, the second fastest growing sector of the economy in terms of GDP growth from 2019-2024 was gambling. Philip Pilkington wrote a good essay last summer on the moral assumptions behind our growth statistics. There is no agreed upon notion of what makes up an economically valuable object or activity, so our stats are inherently subtle moral judgments. Classic moral philosophers like Adam Smith believed in the “use value” of an item, meaning how it could be used, whereas neoclassical economists believed in the “exchange value” of an item, making no judgments about use and are just counting up its market price.

Normal people subscribe on a moral level to use value. Most of us see someone spending money on a gambling addiction as doing something worse than providing Christmas presents for kids, but not because of price. However, our GDP models use the market value basis. Kuznets, presumably, was not amoral, he just thought that our laws would ban immoral activities like gambling, and so use value and market value wouldn’t diverge. But they have.

It’s not just things like gambling or pornography or speculation. A lot of previously unmeasured activity has been turned into data and monetized, which isn’t actually increasing real growth but measuring what already existed. Take the change from meeting someone at a party to using a dating app. One is part of GDP, the other isn’t. Both are real, but only one would show a bigger economy.

Beyond that much of our economy is now based on intangibles – the fastest growing sector was software publishing. Is Microsoft moving to a subscription fee model for Office truly some sort of groundbreaking new product? It’s hard to say, while corporate assets used to be hard things like factories, today much of it is intangibles like intellectual property.

A boomcession, where the rich and corporate America experience a boom while working people feel a recession, is a very unhealthy dynamic. It’s certainly possible to create metrics to measure it, and to help policymakers understand real income growth among different subgroups. You could start looking at real income after non-discretionary consumer spending, or find ways of adjusting for price discrimination.

But I think a better approach is to try to knit us into one society again. The kinds of policymakers who could try to create metrics to understand the different experiences of classes, and ameliorate them, don’t have power. Instead, the people in charge still use models which presume one economy and one relatively uniform set of prices, where “consumer spending” means stuff consumers want.

I once noted a speech in 2016 by then-Fed Chair Janet Yellen in which she expressed surprise that powerful rich firms and small weak ones had different borrowing rates, which affected the “monetary transmission channel” the Fed relied on. Sure it was obvious in the real world, but she preferred theory.

Or they don’t use models at all; Kevin Warsh is not an economist, he’s a lawyer and political operative, and is uninterested in academic theory. He cares about corporate profits and capital formation. That probably won’t work out well either.

At any rate, we have to start measuring what matters again. If we don’t, then we’ll continue to be baffled that normal people hate the economy that looks fine on our charts…

The models used by policymakers to understand wages, economic growth, and consumer spending are misleading. That’s why corporate America is having a party, and everyone else is mad. Eminently worth reading in full: “The Boomcession: Why Americans Hate What Looks Like an Economic Boom,” from @matthewstoller.bsky.social (or @mattstoller.skystack.xyz).

* Richard Hamming (and also to the article above, see “Goodhart’s law“)

###

As we ponder the pecuniary, we might recall that it was on this date in 1958 that Benelux Economic Union was founded, creating the seed from the European Economic Community, then the European Union grew.

On that same day, Philadelphia doo wop group The Silhouettes started five weeks at the top of the Billboard R&B chart with their first single, “Get A Job.”

“Location, location, location”*…

Adam Tooze on the biggest vulnerability in the global economy…

In this precarious moment – in the fourth quarter of 2022, two years into the recovery from COVID – of all the forces driving towards an abrupt and disruptive global slowdown, by far the largest is the threat of a global housing shock…

In the global economy there are three really large asset classes: the equities issued by corporations ($109 trillion); the debt securities issued by corporations and governments ($123 trillion); and real estate, which is dominated by residential real estate, valued worldwide at $258 trillion. Commercial real estate ($32.6 trillion) and agricultural land add another $68 trillion. If economic news were reported more sensibly, indices of global real estate would figure every day alongside the S&P500 and the Nasdaq. The surge in global house prices in 2019-2021 added tens of trillions to measured global wealth. If that unwinds it will deliver a huge recessionary shock.

In regional terms, as a first approximation, think of global real estate assets as split four ways, with the US, China and the EU each accounting for c. 20-22 percent and 35 percent or so belonging to the rest of the world.

The housing complex is at the heart of the capitalist economy. Construction is a major industry worldwide. It is one of the classic drivers of the business-cycle. But beyond the constructive industry itself, the influence of housing as an asset class is pervasive. Compared to equities or debt securities, residential real estate is owned in a relatively decentralized way. Homeownership defines the middle class. And for the majority of households in that class, those with any measurable net worth, the home is the main marketable asset.

Middle-class households are for the most part undiversified and unhedged speculators in one asset, their home. Furthermore, since homes are the only asset that most households can use as collateral, they pile on leverage. For households, as for firms, leverage promises outsized gains, but also brings with it serious risks in the event of a downturn. Mortgage and rental payments are generally the largest single item in household budgets. And household spending, which accounts for 60 percent of GDP in a typical OECD member, is also responsive to perceived household wealth and thus to home equity – the balance between home prices and the mortgages secured on it. For all of these reasons, a surge in mortgage rates and/or a slump in house prices is a very big deal for the world economy and for society more generally…

More background and an assessment of the outlook: “The global housing downturn,” from @adam_tooze.

For Tooze’s follow-up piece on the risk inherent in the $23 trillion US Treasury market, see here.

###

As we mortgage our futures, we might recall that it was on this date in 1914 that the Federal Reserve Bank of the U.S. was opened. In actuality a network of 12 regional banks, joined in the Federal Reserve System, they oversee federally-chartered banks in their regions and are jointly responsible for implementing the monetary policy set forth by the Federal Open Market Committee.

In that latter role, they are central to the housing market in that they set interest rates and purchase mortgage securities from Fannie Mae and Freddie Mac (Government-Sponsored Enterprises in the mortgage market). At this point the Fed owns about a quarter of the mortgage-backed securities issued by Fannie Mae and Freddie Mac.

The Federal Reserve Banks in 1936 (source)

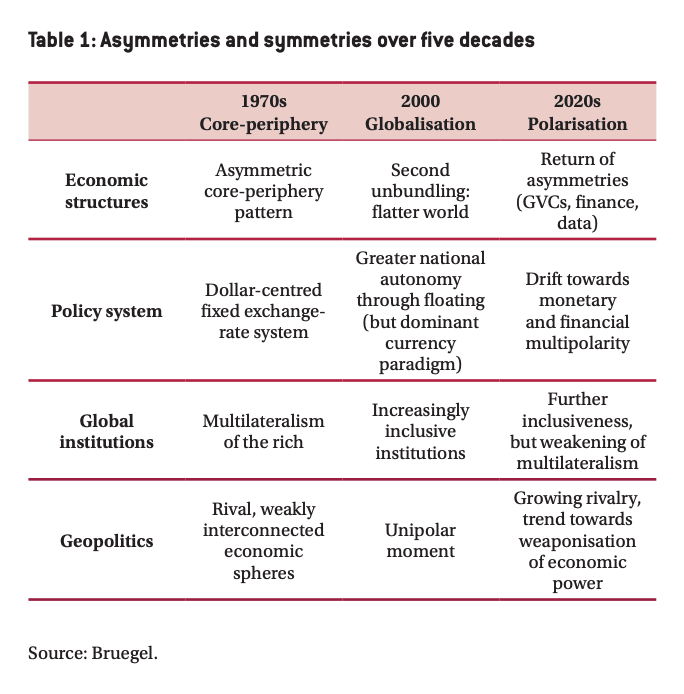

“Symmetry is not the way of the world in all times and places”*…

What a difference a couple of decades make…

Asymmetries are back. Rising market power, the sudden ubiquity of global digital networks, hierarchical hub-and-spoke structures in international trade and finance and the enduring dominance of the US dollar, despite the transition to floating exchange rates, all point to their resurgence. The remarkable decay of economic multilateralism in the very fields – trade and development finance – where global rules and institutions were first tried and reigned supreme for decades, is paving the way to a redefinition of international relations on a bilateral or regional basis, with powerful countries setting their own rules of the game. This transformation is compounded by the strengthening of geopolitical rivalry between the US, China and a handful of second-tier powers.

Donald Trump’s attempt to leverage US centrality in the global economy to extract rents from economic partners was short-lived. But US policy has certainly changed permanently. For all its friendly intentions, the Biden administration leaves no doubt about its overriding priorities: a foreign policy for the (domestic) middle class – to quote the title of a recent report (Ahmed et al, 2020) – and the preservation of the US edge over China. China, for its part, has set itself the goal of becoming by 2049 a “fully developed, rich and power-ful” nation and does not show any intention to play by multi-lateral rules that were conceived by others. In this context, the rapid escalation of great power competition between Washington and Beijing is driving both rivals towards the building of competing systems of bilateral or regional arrangements.

What is emerging is not only an asymmetric hub-and-spoke landscape. It is a world in which hubs are controlled by major geopolitical powers – in other words, a multipolar, fragmented world. Nothing indicates that these asymmetries will fade away any time soon. On the contrary, economic, systemic and geopolitical factors all suggest they may prove persistent. We will have to learn to live with them.

There are several consequences. First, this new context calls for an analytical reassessment. Recent research has put the spotlight on a series of economic, financial or monetary asymmetries and has begun to uncover their determinants and effects. Analytical and empirical tools are available that make it possible to gather systematic evidence and to document the impact of asymmetries on the distribution of the gains from economic interdependence. We are on our way to learning more about the welfare and the policy implications of participating in an increasingly asymmetric global system.

Second, the relationship between economics and geopolitics must now be looked at in a more systematic way. For many years – even before the demise of the Soviet Union – international economic relations were considered in isolation, at least by economists. They were looked at as if they were (mostly) immune from geopolitical tensions. This stance is no longer tenable, at a time when great-power rivalry is reasserting itself as a key determinant of policy decisions. Whatever their wishes, economists have no choice but to respond to this new reality. They should document the potential for coercion by powers in control of crucial nodes or infrastructures and the risks involved in participating in the global economy from a vulnerable position.

Third, supporters of multilateralism need to wake up to the new context. They have too often championed a world made up of peaceful and balanced relations that bears limited resemblance to reality. Because power and asymmetry can only be forgotten at one’s own risk, neglecting them inevitably fuels mistrust of principles, rules and institutions that are perceived as biased. Multilateralism remains essential, but institutions are not immune to the risk of capture.

Asymmetry, however, does not imply a change of paradigm. Even if it affects the distribution of gains from trade, it does not abolish them. And in a world in which global public goods (and bads) have moved to the forefront of the policy agenda, there is no alternative to cooperation and institutionalised collective action. The prevention of climate-related disasters, maintenance of public health and preservation of biodiversity will remain vital tasks whatever the state of inter-national relations. What asymmetries call for is an adaptation of policy template. The multilateral project should not be ditched, but it must be rooted in reality.

Understanding the emerging new global economy: from the conclusion of Jean Pisani-Ferry‘s (@pisaniferry) paper, “Global Assymetries Strike Back,” eminently worth reading in full. [Via @adam_tooze]

* Charles Kindelberger, economic historian and architect of the Marshall Plan

###

As we find our place, we might send tight birthday greetings to Paul Adolph Volcker Jr.; he was born on this date in 1927. An economist, he was appointed Federal Reserve Chair by President Carter in 1979, and reappointed by President Reagan. He took that office in a time of “stagflation” in the U.S.; his tight money policies, combined with Reagan’s expansive fiscal policy(large tax cuts and a major increase in military spending), tamed inflation, but led to much larger federal deficits (and thus, higher federal interest costs) and increased economic imbalances across the economy. In the end, Reagan let Volcker go; as Joseph Stiglitz observed, “Paul Volcker… known for keeping inflation under control, was fired because the Reagan administration didn’t believe he was an adequate de-regulator.”

Volcker returned to government service in 2009 as the chairman of President Obama’s Economic Recovery Advisory Board. In 2010, Obama proposed bank regulations which he dubbed “The Volcker Rule,” which would prevent commercial banks from owning and investing in hedge funds and private equity, and limit the trading they do for their own accounts (a reprise of a key element in the then-defunct Glass-Steagell Act). It was enacted; but in 2020, FDIC officials said the agency would loosen the restrictions of the Volcker Rule, allowing banks to more easily make large investments into venture capital and similar funds.

“A fair day’s-wage for a fair day’s work: it is as just a demand as governed men ever made of governing.”*…

As low-wage employers struggle to find workers, it seems as that labor– which has been left behind over the last several decades, as the economic benefits of growth have flowed to executives and owners– may be about to have its day. But will it? And what might that mean?

In her first statement as Treasury Secretary, Janet Yellen said that the United States faced “an economic crisis that has been building for fifty years.” The formulation is intriguing but enigmatic. The last half century is piled so high with economic wreckage that it is not obvious how to name the long crisis, much less how to pull the fragments together into a narrative. One place to start is with the distribution of national income between labor and capital (or, looked at another way, between the wage share and the profit share of national income). About fifty years ago, the share of income going to labor began to decline, forming a statistical record of the epochal collapse of working class power. Episodes of high employment in the 1990s and the late 2010s did not reverse the long-term pattern. Even today, with a combination of easy money and fiscal stimulus unprecedented since World War II, it is unclear what it would take to reverse the trend in distribution.

Few would seriously dispute that hawkish Federal Reserve policies have played a direct role in the decline of the labor share since the 1970s. This is the starting point for thinking about monetary policy and the income distribution, but many questions remain. Today’s expansionary program extends beyond monetary policy to include fiscal stimulus and even industrial policy, but the first sign of an elite rethinking was the Fed’s dovish turn around 2016. (The Fed chair then was Yellen, whose current tenure as Treasury Secretary has been marked by close coordination with her successor, Jerome Powell.) In a fundamental sense, the entire Biden program hangs on the Fed: low interest rates made possible a reevaluation of the cost of massive government debt, which has in turn opened new horizons for a would-be activist government.

If the age of inequality was the product of a hawkish Fed, could a dovish central bank reverse the damage? Today, there is more reason to speak of a “pro-labor turn” than perhaps at any time over the last half century. But history is not so easily reversed. The new policy regime is not a simple course correction to decades of misguided neoliberalism. There is evidence that the current experiment was made possible by a recognition that workers had suffered a secular defeat—specifically, that they had lost the ability to increase or even defend their share of the national income. What would happen if labor became stronger?…

Tim Barker (@_TimBarker) explores: “Preferred Shares,” in Phenomenal World (@WorldPhenomenal).

On a related note: “The economics of dollar stores.”

[Image above: source]

* Thomas Carlyle

###

As we re-slice the pie, we might send acquisitive birthday greetings to Claude-Frédéric Bastiat; he was born on this date in 1801 (though some sources give tomorrow as his birthday). An economist and writer, he was a prominent member of the French Liberal School. As an advocate of classical economics and the views of Adam Smith, his advocacy for free markets influenced the Austrian School; indeed, Joseph Schumpeter called him “the most brilliant economic journalist who ever lived”… which is to say that Bastiat was a father of the neo-liberal economic movement that’s been central to creating the situation we’re in.

“The essence of investment management is the management of risks, not the management of returns”*…

In 1754, the infamous scam artist, diarist, and womanizer Giacomo Girolamo Casanova reported that a certain type of high-stakes wager had come into vogue at the Ridotto. The bet was known as a martingale, which we would immediately recognize as a rather basic coin toss. In a matter of seconds, the martingale could deliver dizzying jackpots or, equally as often, ruination. In terms of duration, it was the equivalent of today’s high-speed trade. The only extraordinary fact about the otherwise simple martingale was that everybody knew the infallible strategy for winning: if a player were to put money on the same outcome every time, again and again ad infinitum, the laws of probability dictated that not only would he win back all he may have previously lost, he would double his money. The only catch was that he would have to double down each time, a strategy that could be sustained only as long as the gambler remained solvent. On numerous occasions, martingales left Casanova bankrupt.

In modern finance, the coin toss has come to represent a great deal more than heads or tails. The concept of the martingale is a bulwark of what economists call the efficient-market hypothesis, the meaning of which can be grasped by an oft-repeated saying on Wall Street: for every person who believes a stock will rise—the buyer—there will be some other equal and opposite person who believes the stock will fall—the seller. Even as markets go haywire, brokers and traders repeat the mantra: for every buyer, there is a seller. But the avowed aim of the hedge fund, like the fantasy of a coin-tosser on the brink of bankruptcy, was to evade the rigid fifty-fifty chances of the martingale. The dream was heads I win, tails you lose.

One premonition as to how such hedged bets could be constructed appeared in print around the time when gambling reached an apex at the Ridotto casino, when an eighteenth-century financial writer named Nicolas Magens published “An Essay on Insurances.” Magens was the first to specify the word “option” as a contractual term: “The Sum given is called Premium, and the Liberty that the Giver of the Premium has to have the Contract fulfilled or not, is called Option . . .” The option is presented as a defense against financial loss, a structure that would eventually make it an indispensable tool for hedge funds.

By the middle of the next century, large-scale betting on stocks and bonds was under way on the Paris Bourse. The exchange, located behind a panoply of Corinthian columns, along with its unofficial partner market, called the Coulisse, was clearing more than a hundred billion francs that could change volume, speed, and direction. One of the most widely traded financial instruments on the Bourse was a debt vehicle known as a rente, which usually guaranteed a three-per-cent return in annual interest. As the offering dates and interest rates of these rentes shifted, their prices fluctuated in relationship to one another.

Somewhere among the traders lurked a young man named Louis Bachelier. Although he was born into a well-to-do family—his father was a wine merchant and his maternal grandfather a banker—his parents died when he was a teen-ager, and he had to put his academic ambitions on hold until his adulthood. Though no one knows exactly where he worked, everyone agrees that Bachelier was well acquainted with the workings of the Bourse. His subsequent research suggests that he had noted the propensity of the best traders to take an array of diverse and even contradictory positions. Though one might expect that placing so many bets in so many different directions on so many due dates would guarantee chaos, these expert traders did it in such a way as to decrease their risk. At twenty-two, after his obligatory military service, Bachelier was able to enroll at the Sorbonne. In 1900, he submitted his doctoral dissertation on a subject that few had ever researched before: a mathematical analysis of option trading on rentes.

Bachelier’s dissertation, “The Theory of Speculation,” is recognized as the first to use calculus to analyze trading on the floor of an exchange, and it contained a startling claim: “I have in fact known for several years that it would be possible . . . to imagine transactions where one of the parties makes a profit at all prices.” The best traders on the Bourse knew how to establish an intricate set of positions designed to protect themselves no matter which way or at what speed the market might move. Bachelier’s process was to separate out each element that had gone into the complex of bets at different prices, and write equations for them. His committee, supervised by the renowned mathematician and theoretical physicist Henri Poincaré, was impressed, but it was an unusual thesis. “The subject chosen by M. Bachelier is rather far away from those usually treated by our candidates,” the report noted. For work that would unleash billion-dollar torrents into the capital pools of future hedge funds, Bachelier received a grade of honorable instead of très honorable. It was a B.

Needless to say, Bachelier’s views of math’s application to finance [published in 1900] were ahead of his time. The implications of his work were not appreciated, much less exploited, by Wall Street until the nineteen-seventies, after his dissertation was discovered by the Nobel Prize winner Paul Samuelson, the author of one of the best-selling economics textbooks of all time, who pushed for its translation into English. Two economists, Fischer Black and Myron Scholes, read the work and, in a 1973 issue of the Journal of Political Economy, published one of the most famous articles in the history of quantitative finance.

Based on Bachelier’s dissertation, the economists developed the eponymous Black-Scholes model for option pricing. They established that an option could be priced from a set-in-stone mathematical equation, which allowed the Chicago Board Options Exchange (C.B.O.E.), a new organization, to expand their business to a new universe of financial derivatives. Within a year, more than twenty thousand option contracts were changing hands each day. Four years after that, the C.B.O.E. introduced the “put” option—thus institutionalizing the bet that the thing you were betting on would lose. “Profit at all prices” had joined the mainstream of both economic theory and practice…

From the remarkable story of the French dissertation that inspired the strategies that guide many modern investors ad al that it has wrought: “A Brief History of the Hedge Fund.”

Spoiler alert: it hasn’t always worked out so well (c.f. Long-Term Capital Management)… at least for investors. As Janet M. Tavakoli observed in Structured Finance and Collateralized Debt Obligations: New Developments in Cash and Synthetic Securitization

Hedge funds have made massive leveraged credit bets, knowing that their upside is billions in fees and their downside is millions in fees.

###

As we ruminate on risk, we might recall that it was on this date in 2020 that the Federal Reserve rode in to rescue financial markets to prevent their complete freezing up– which could have entered history books as another global mega-crash. The Dow Jones stock market index had hit an all-time record of 29,551 on February 12, 2020. Then, the coronavirus emerged in earnest in the U.S., unemployment soared, and on March 9 the DJIA took a dive of over 2,000 points; it continued to fall, down to 18,321 on March 23… at which point the Fed intervened, pouring vast sums of cash into the financial system, resulting in a stock market bonanza in the midst of the worst economic collapse since the Great Depression. The Dow stands at this writing at over 35,000.

You must be logged in to post a comment.