Posts Tagged ‘stagflation’

“Symmetry is not the way of the world in all times and places”*…

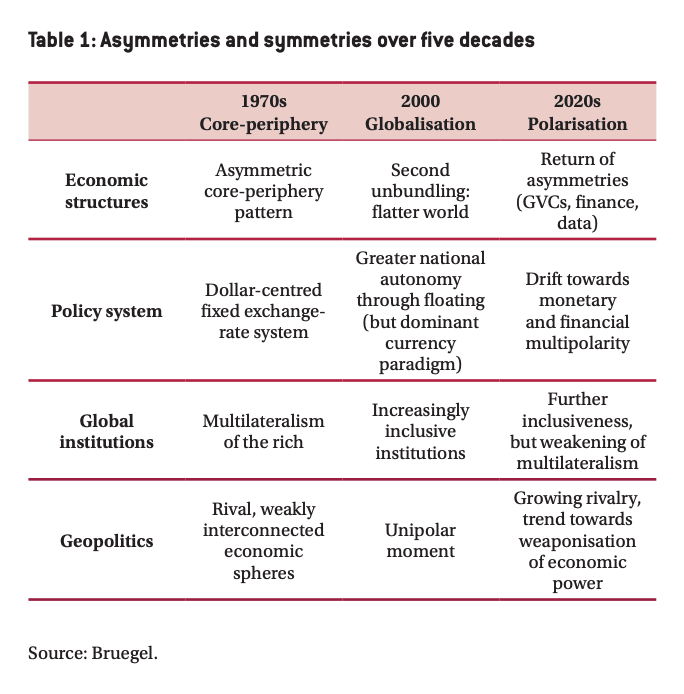

What a difference a couple of decades make…

Asymmetries are back. Rising market power, the sudden ubiquity of global digital networks, hierarchical hub-and-spoke structures in international trade and finance and the enduring dominance of the US dollar, despite the transition to floating exchange rates, all point to their resurgence. The remarkable decay of economic multilateralism in the very fields – trade and development finance – where global rules and institutions were first tried and reigned supreme for decades, is paving the way to a redefinition of international relations on a bilateral or regional basis, with powerful countries setting their own rules of the game. This transformation is compounded by the strengthening of geopolitical rivalry between the US, China and a handful of second-tier powers.

Donald Trump’s attempt to leverage US centrality in the global economy to extract rents from economic partners was short-lived. But US policy has certainly changed permanently. For all its friendly intentions, the Biden administration leaves no doubt about its overriding priorities: a foreign policy for the (domestic) middle class – to quote the title of a recent report (Ahmed et al, 2020) – and the preservation of the US edge over China. China, for its part, has set itself the goal of becoming by 2049 a “fully developed, rich and power-ful” nation and does not show any intention to play by multi-lateral rules that were conceived by others. In this context, the rapid escalation of great power competition between Washington and Beijing is driving both rivals towards the building of competing systems of bilateral or regional arrangements.

What is emerging is not only an asymmetric hub-and-spoke landscape. It is a world in which hubs are controlled by major geopolitical powers – in other words, a multipolar, fragmented world. Nothing indicates that these asymmetries will fade away any time soon. On the contrary, economic, systemic and geopolitical factors all suggest they may prove persistent. We will have to learn to live with them.

There are several consequences. First, this new context calls for an analytical reassessment. Recent research has put the spotlight on a series of economic, financial or monetary asymmetries and has begun to uncover their determinants and effects. Analytical and empirical tools are available that make it possible to gather systematic evidence and to document the impact of asymmetries on the distribution of the gains from economic interdependence. We are on our way to learning more about the welfare and the policy implications of participating in an increasingly asymmetric global system.

Second, the relationship between economics and geopolitics must now be looked at in a more systematic way. For many years – even before the demise of the Soviet Union – international economic relations were considered in isolation, at least by economists. They were looked at as if they were (mostly) immune from geopolitical tensions. This stance is no longer tenable, at a time when great-power rivalry is reasserting itself as a key determinant of policy decisions. Whatever their wishes, economists have no choice but to respond to this new reality. They should document the potential for coercion by powers in control of crucial nodes or infrastructures and the risks involved in participating in the global economy from a vulnerable position.

Third, supporters of multilateralism need to wake up to the new context. They have too often championed a world made up of peaceful and balanced relations that bears limited resemblance to reality. Because power and asymmetry can only be forgotten at one’s own risk, neglecting them inevitably fuels mistrust of principles, rules and institutions that are perceived as biased. Multilateralism remains essential, but institutions are not immune to the risk of capture.

Asymmetry, however, does not imply a change of paradigm. Even if it affects the distribution of gains from trade, it does not abolish them. And in a world in which global public goods (and bads) have moved to the forefront of the policy agenda, there is no alternative to cooperation and institutionalised collective action. The prevention of climate-related disasters, maintenance of public health and preservation of biodiversity will remain vital tasks whatever the state of inter-national relations. What asymmetries call for is an adaptation of policy template. The multilateral project should not be ditched, but it must be rooted in reality.

Understanding the emerging new global economy: from the conclusion of Jean Pisani-Ferry‘s (@pisaniferry) paper, “Global Assymetries Strike Back,” eminently worth reading in full. [Via @adam_tooze]

* Charles Kindelberger, economic historian and architect of the Marshall Plan

###

As we find our place, we might send tight birthday greetings to Paul Adolph Volcker Jr.; he was born on this date in 1927. An economist, he was appointed Federal Reserve Chair by President Carter in 1979, and reappointed by President Reagan. He took that office in a time of “stagflation” in the U.S.; his tight money policies, combined with Reagan’s expansive fiscal policy(large tax cuts and a major increase in military spending), tamed inflation, but led to much larger federal deficits (and thus, higher federal interest costs) and increased economic imbalances across the economy. In the end, Reagan let Volcker go; as Joseph Stiglitz observed, “Paul Volcker… known for keeping inflation under control, was fired because the Reagan administration didn’t believe he was an adequate de-regulator.”

Volcker returned to government service in 2009 as the chairman of President Obama’s Economic Recovery Advisory Board. In 2010, Obama proposed bank regulations which he dubbed “The Volcker Rule,” which would prevent commercial banks from owning and investing in hedge funds and private equity, and limit the trading they do for their own accounts (a reprise of a key element in the then-defunct Glass-Steagell Act). It was enacted; but in 2020, FDIC officials said the agency would loosen the restrictions of the Volcker Rule, allowing banks to more easily make large investments into venture capital and similar funds.

You must be logged in to post a comment.